If there is one word that defines the U.S. agricultural economy in early 2026, it’s confidence, or more precisely, the lack of it. It’s not just an eroding confidence in data, but declining confidence in policy and whether the traditional tools used to stabilize farm income still work.

The first Farm Journal Ag Economists’ Monthly Monitor of 2026, coupled with input from producers and ag retailers, reveals an industry that broadly agrees it is in trouble, but sharply disagrees on why, who should fix it and how farmers will survive it.

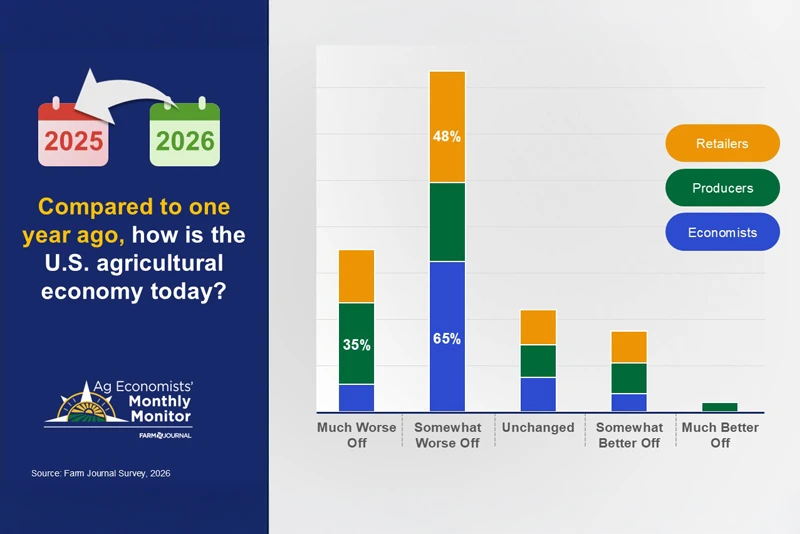

Across the economists, farmers and retailers surveyed, the results paint a picture of a crop sector stuck in recession, magnified by the squeeze caused by high input costs and low commodity prices.

Factors Driving the Health of the Ag Economy Today

Economists in January’s survey pointed to a familiar but intensifying split in the ag economy: strength in livestock, particularly beef cattle, versus persistent financial stress across much of the row-crop sector. Tight cattle supplies and strong global demand for animal protein continue to support profitability in the livestock sector, even as economists warn that future prospects remain uncertain. At the same time, global surpluses of corn, soybeans and wheat, combined with weak export demand for certain commodities, are weighing heavily on crop prices.

Across nearly all responses, margin pressure emerged as a dominant concern. Elevated input costs, rising interest rates and tightening access to operating loans are pushing break-even costs above market prices for many producers, especially in grain production.

Economists repeatedly cited policy uncertainty, ranging from trade relations to biofuels policy, as a pivotal factor. While government assistance and expectations of additional ad hoc payments are providing some near-term relief, many note those funds are largely being used to service debt rather than reinvest in operations, underscoring ongoing liquidity challenges in farm country.

In the anonymous survey, when asked the two factors driving the health of the ag economy today, the economists said:

- “Continued strength in the cattle business and that the world is awash in corn, wheat and soybeans.”

- “Cost-price margins: Agriculture’s economic health is being driven first by whether commodity prices are high enough to cover still-elevated input, labor and operating costs.”

- “Policy uncertainty hurting export demand and biofuels demand — cattle receipts providing lucrative returns but with uncertain future prospects.”

- “Break-even costs above market prices, demand uncertainty on multiple fronts.”

- “Persistent high input costs and uncertainty regarding trade, particularly trade with China.”

- “Access to operating loans and the amount of debt producers are carrying from the previous two years of down revenue.”

- “Positives include strong beef cattle margins and relatively stable land prices; negatives are burdensome crop supplies, high input prices and very low liquidity.”

A Crop Sector in Recession By Consensus

On the state of the economy itself, there is little debate:

- 76% of economists say the U.S. crop sector is in a recession.

- 74% of producers agree.

- More than 76% of economists believe conditions are worse than a year ago.

Economists warn this environment is accelerating consolidation, with 72% expecting low prices and high costs to push weaker operations out of the market with 80% of retailers saying it will increase consolidation in the industry.

When you look at what’s preventing profitability, high input costs remain the dominant hurdle for producers:

- 67% of producers cite input prices as their biggest obstacle.

- 62% of economists agree that high input costs are a hurdle for farmers in 2026.

Sticky costs for fertilizer, labor, interest rates and materials, combined with soft commodity prices, have pushed many producers to sell at or below break-even.

“Maximum Is Rarely Optimum:” How Farmers Say They’ll Stay Alive and Competitive in 2026

When asked a simple but heavy question: “What can you do to be successful in 2026,” farmers didn’t sugarcoat the challenge. Their answers reflect pressure, fatigue and uncertainty. But underneath the blunt language is a clear, consistent strategy emerging across operations: protect cash, defend ROI and stay flexible long enough to outlast the cycle.

While several producers said they’re looking to diversify as a key to success, the most dominant theme was cutting costs to the bone, especially when it comes to capital spending. Farmers repeatedly emphasized zero, or near-zero, capex, delaying equipment upgrades and scrutinizing every purchase.

The mindset is not panic, but discipline. In this month’s survey, farmers said the key to success is:

- “Zero capital spending or as close to zero as possible.”

- “Don’t buy anything that isn’t absolutely necessary.”

- “Hold off on major capital expenditures.”

- “Ask yourself before you purchase something, is it a want or a need. Wants can break you fast.”

Many farmers framed this as a return to fundamentals: preserving working capital, maintaining flexibility, and avoiding irreversible decisions in an uncertain margin environment.

The Federal Aid Gap: Band-Aid or Lifeline?

Few issues expose the disconnect between economists and producers more clearly than federal aid.

There is broad agreement on one point: Ad hoc farm payments are not a long-term solution. Just under 60% of both economists and producers describe them as “a Band-Aid that won’t heal the wound.”

Beyond that, thoughts on federal aid differ.

- 51% of producers believe more than $20 billion in additional aid is required to stabilize the ag economy.

- 28% of economists believe no additional aid is needed at all while the remainder are split across ranges from $11 billion to $20 billion.

This gap matters because it directly influences behavior. Both groups agree that government policy will be a major driver of planting decisions in 2026, with a clear bias toward corn. Expectations around payments, programs and biofuels demand are shaping acres before a seed ever goes in the ground.

Biofuels: One Industry, Two Visions of Salvation

No policy area reveals the philosophical divide between “on the ground” agriculture and “on the spreadsheet” analysis more clearly than biofuels. Producers want more demand now, whereas economists are looking five to 10 years out.

Producers and retailers overwhelmingly prioritize E15 expansion, viewing it as the single fastest way to generate real, immediate demand for corn and reduce reliance on government support.

Economists, while supportive of E15, are more focused on structural, longer-term demand drivers, particularly:

- 45Z tax credit

- Development of Sustainable Aviation Fuel (SAF) markets

Among economists, 39% ranked the 45Z tax credit as the most impactful policy, while SAF ranked much higher than it did among producers where 44% ranked SAF as least impactful.

The Collapse of Trust in USDA Data

USDA’s January Crop Production Report was a point of contention last month. With much debate about the validity of the latest yield, acreage and production data from USDA, Farm Journal’s January survey results is the near-universal erosion of trust in USDA data, not only among producers, but also economists and retailers.

- 68% of economists say they are not as confident in USDA reporting as they were in the past.

- 73% of producers agree.

- 78% of retailers say their confidence in USDA has waned.

For economists, the concern centers on revisions, lagging indicators and the challenge of modeling markets amid policy uncertainty. For producers, the distrust is far more emotional and personal. Open-ended responses frequently referenced “market manipulation,” “bearish curveballs” and a sense that official numbers no longer reflect what’s happening at the farm gate.

In a market environment already defined by thin margins, the loss of confidence in baseline data further complicates marketing, risk management and lending decisions. When trust in the numbers erodes, so does the ability to plan.

Political Support Remains, But Confidence Is Slipping

One year into the Trump administration, producers remain broadly supportive of the president. But confidence in Washington’s ability to improve the ag economy is fading.

- 52% of economists say they are less confident the administration can improve agriculture.

- 44% of producers report declining confidence as well.

The divide between the groups is notable. Only 8% of economists feel more confident than a year ago, while 34% of producers say their confidence has increased, suggesting optimism on the farm still exists, even as economists grow more skeptical.

Trade uncertainty, shifting biofuels policy signals and questions about the future of ad hoc aid have all contributed to a sense that political alignment does not automatically translate into economic relief.

Strategy vs. Survival

Where the survey becomes most revealing is in the open-ended responses about survival. Economists see a severe but cyclical downturn. Many producers see a structural breaking point.

Economists speak the language of optimization. Their recommendations include:

- Margin-first decision-making

- Defensive marketing

- Strategic planning

- Focusing on high-productivity acres

- Driving down per-unit input costs

Producers speak the language of survival, saying the key to weathering this story will be:

- “Find an off-farm job”

- “Send my spouse back to work”

- “Sell out”

Some responses went further, referencing bankruptcy and financial collapse, a level of personal desperation absent from economists’ professional analysis.

One producer wrote: “I am facing financial crisis and homelessness … in the worst financial situation ever.”

An economist, by contrast, said: “Key to profitability lies in driving input costs down… a shift from maximizing inputs to optimization.”

Navigating 2026: From Maximum Yield to Maximum ROI

Despite the pressure, confidence in farmers themselves remains surprisingly strong.

Between 62% and 80% of respondents believe producers will find a way through, by abandoning the long-held pursuit of maximum yield in favor of maximum return on investment.

How that transition looks will vary, according to economists and producers, including:

- More defensive marketing

- Reduced input intensity

- Greater scrutiny of every acre

- More off-farm income

- Tough conversations with lenders

The 2026 ag economy will not be defined by a single policy fix or market rally. It will be shaped by trust, or the lack of it, by how quickly demand can be grown without government intervention and by how much pain producers can absorb before the structure of the industry permanently changes.

Bottom Line for the Ag Industry

The U.S. ag economy enters 2026 in a clear crop-sector recession, but the deeper crisis is one of confidence. High input costs, weak prices, policy uncertainty and eroding trust in data have pushed many producers from planning for profitability into fighting for survival. Economists largely view the downturn as cyclical and manageable through optimization, while farmers experience it as a structural stress test on their operations and livelihoods.

How 2026 ultimately unfolds will depend less on short-term aid and more on rebuilding trust, growing demand without permanent government support and farmers’ ability to preserve cash, adapt quickly and endure a prolonged margin squeeze.