Crude Oil Prices Hit Six-Month High on Worries About Israel/Iran Conflict

Robust jobs report | Timeline to reopen Port of Baltimore | Fedspeak | Ag trade | No tax bill

|

Today’s Digital Newspaper |

MARKET FOCUS

- Job growth in March easily surpasses pre-report expectations

- Neel Kashkari floats possibility of no rate cuts in 2024, but…

- Loretta Mester suggested the Fed may be near the confidence to start easing, but…

- Patrick Harker and Thomas Barkin says CPI too high and there’s time to assess data

- European Central Bank expected to maintain interest rates

- $90 Brent crude oil… $100 ahead?

- Gold performing better than S&P 500

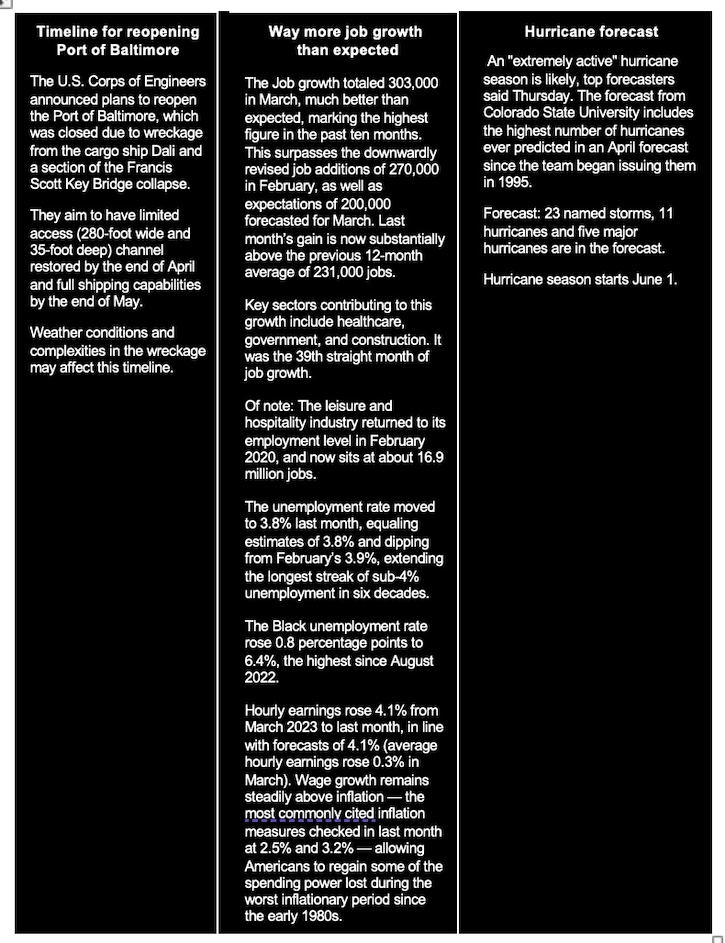

- U.S. Corps of Engineers announces plans to reopen Port of Baltimore

- SEC stays implementation of climate reporting rule due to ongoing judicial reviews

- Ford to postpone production of a new all-electric large SUV and pickup truck

- Apple plans to lay off 614 employees in California after shutting down its car project

- Samsung Electronics estimates operating profits surged by 931% year on year

- Checking Biden and Trump on manufacturing jobs

- Ag markets today

- Detection of avian influenza in dairy cows spooks cattle markets

- In February, rise in ag exports helped narrow monthly trade deficit in U.S.

- USDA's NASS unveils changes to livestock reports based on five-year review

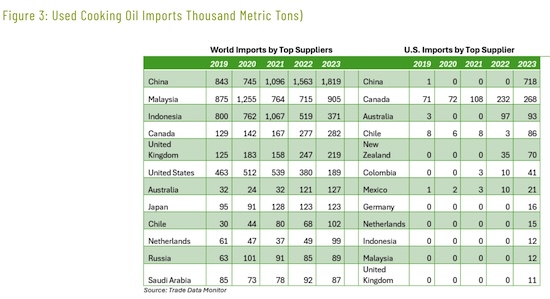

- Biomass-based diesel surges as used cooking oil imports rise… regulatory concerns

- Ag trade update

- Forecast for upcoming Atlantic hurricane season predicts ‘extremely active’ season

- NWS weather outlook

- Pro Farmer First Thing Today items

BALTIMORE BRIDGE COLLAPSE

- U.S. Corps of Engineers announces plans to reopen Port of Baltimore

- President Joe Biden will visit Baltimore today

- White House: Congress should fully repair costs to Baltimore’s collapsed bridge

- 11 cargo ships, including four crucial for national defense, stuck behind wreckage

- Challenge due to presence of high-pressure natural gas pipeline running beneath it

CONGRESS

- House Ways and Means Committee to address future tax policy in April 11 hearing

- Senate Republicans poised to block $78 billion tax-cut package

ISRAEL/HAMAS CONFLICT

- Biden tells Netanyahu strikes on aid workers are ‘unacceptable’; insists on cease fire

- Israel to open new border crossing in northern Gaza to increase aid delivery

RUSSIA & UKRAINE

- Two RIF Russian grain cargoes receive phytosanitary certificates

CHINA

- Argentine President Milei's shift on China

- Brookings: How will Biden and Trump tackle trade with China?

LIVESTOCK, NUTRITION & FOOD INDUSTRY

- FAO food price index ends prolonged slide in March

- New cases of HPAI confirmed in Ohio, bringing total number of states affected to six

- Hype or legit concern? Bird flu pandemic could be ‘100 times worse’ than Covid

- Iowa House passes food labeling bill amid egg substitute purchase restrictions

POLITICS & ELECTIONS

- No Labels abandoned its potential third-party presidential bid

- Bill Clinton to publish memoir about life after White House

- Charlie Cook: Dems “firewall" hinges on winning back control of House

OTHER ITEMS OF NOTE

- Cotton AWP falls under 70 cents

- NCGA opposes Corteva's petition for duties on herbicide 2,4-D from India and China

|

MARKET FOCUS |

— Equities today: Asian and European stock indexes were mostly lower overnight. U.S. Dow opened slightly higher. In Asia, Japan -2%. Hong Kong flat. China closed. India flat. In Europe, at midday, London -1%. Paris -1.4%. Frankfurt -1.4%.

U.S. equities yesterday: All three major indices finished with losses of more than 1.2% Thursday ahead of the key Employment report due Friday morning. The Dow dropped 530.16 points, 1.35%, at 38,596.98. The Nasdaq fell 228.38 points, 1.40%, at 16,049.08. The S&P 500 declined 64.28 points, 1.23%, at 5,147.21.

— The Securities and Exchange Commission (SEC) has issued an order to stay the implementation of its climate reporting rule due to ongoing judicial reviews. The SEC stated that it is opting to delay the final rule's implementation pending the outcome of cases in the Eighth Circuit Court of Appeals, where multiple petitions from companies, organizations, and states have been consolidated. Despite the stay, the SEC maintains that the final rules are consistent with applicable law and its authority to require disclosure important to investors. The SEC emphasized its commitment to defending the rule's validity in court and anticipates a prompt resolution of the litigation. By staying the rule, the SEC aims to facilitate orderly judicial resolution and prevent regulatory uncertainty during the court challenges. This delay prolongs the potential impact of the rule until the court issues its decision.

— Ford announced on Thursday that it will postpone the production of a new all-electric large SUV and pickup truck. Originally planned for 2025, the production of the three-row SUV will now be delayed until 2027, while the pickup, codenamed "T3," will be pushed back from late 2025 to 2026. Ford's goal is to introduce hybrid options across its North American lineup by 2030. This decision reflects the slower-than-expected adoption of electric vehicles (EVs) and the persistently high production costs associated with them.

— Apple plans to lay off 614 employees in California after shutting down its car project, its biggest round of job cuts since the pandemic.

— Samsung Electronics estimated that its operating profits surged by 931% year on year, to 6.6 trillion won ($4.9 billion), in the first quarter of 2024. The preliminary figures were particularly encouraging at the South Korean conglomerate’s chip division, which recorded its first profit in more than a year. The firm has benefited from strong demand amid an AI boom and rising memory chip prices.

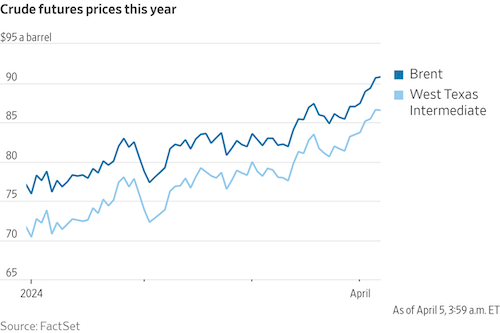

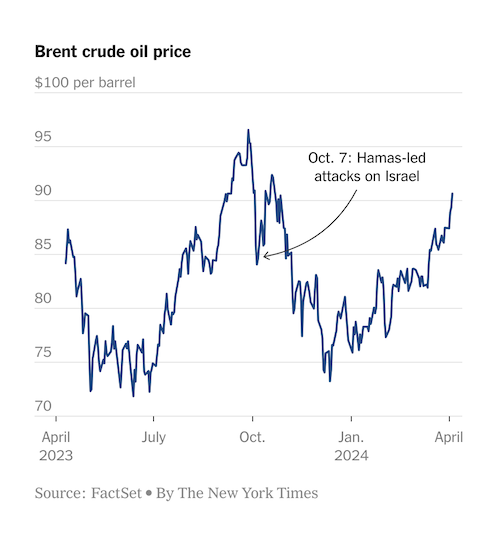

— Crude oil futures: Brent crude, the international benchmark, rose 1.5% to $90.65 a barrel. A widening conflict in the region would endanger supplies of oil, as Iran is one of the Middle East’s largest oil producers. WTI crude, the U.S. standard, settled at $86.59 a barrel. Prices moved higher again early Friday. Brent crude futures have climbed 18% in 2024 to exceed $90 a barrel for the first time since October. That is feeding into gasoline, with average national prices measured by AAA up 15% this year at $3.57 a gallon. “The market in general is only just waking up to just how…tight supplies will increasingly be,” said Paul Horsnell, head of commodities research at Standard Chartered.

— 6.26: Average number of days shipments leaving the ports of Long Beach and Los Angeles waited in February to move by rail, up about 1.5 days from January and the longest dwell time since last September, according to the Pacific Merchant Shipping Association.

— Ag markets today: Corn, soybeans and wheat have adopted firmer tones this morning, led by strong gains in SRW wheat, after two-sided trade overnight. As of 7:30 a.m. CT, corn was trading 2 to 3 cents higher, soybeans were 1 to 3 cents higher, SRW wheat was 12 to 15 cents higher, HRW wheat was 8 to 9 cents higher and HRS wheat was 5 to 7 cents higher. The U.S. dollar index was around 150 points higher, while front-month crude oil futures were near unchanged.

Wholesale beef prices continue to plunge. Wholesale beef prices fell another $4.15 for Choice to $297.15 and 87 cents for Select to $296.05. The Choice/Select spread tightened to an ultra-thin $1.10. While movement improved stayed strong at 162 loads, packers are having to slash prices to encourage retailer buying.

Cash hog index, pork cutout jump. The CME lean hog index is up another 73 cents to $85.88, the biggest daily gain since Feb. 21. The cash index has strengthened $20.83 since the seasonal low at the start of this year. The pork cutout value firmed $3.24 on Thursday, fueled by an $11.53 surge in primal bellies, though all cuts except ribs posted strong daily gains.

— Agriculture markets yesterday:

- Corn: May corn rose 3 1/2 cents to $4.35 1/4, marking a high-range close above the 40- and 10-day moving averages.

- Soy complex: May soybean futures fell 2 1/4 cents to $11.80, well off session lows. May soymeal futures rose $3.50 on late-session strength to $333.50. May bean oil futures dropped 70 points to 48.15 cents.

- Wheat: May SRW wheat closed up 1/4 cent at $5.56 1/4 and nearer the session high. May HRW wheat fell 3 cents to $5.77 1/2 and nearer the session low. May HRS rallied 6 3/4 cents to $6.46 1/4.

- Cotton: May cotton futures plunged 184 points to 87.14 cents, settling on session lows.

- Cattle: June live cattle closed up 25 cents at $175.85 and nearer the session high. The expiring April contract gained 55 cents to $181.475. May feeder cattle gained $1.30 to $243.875 and nearer the daily high.

- Hogs: Continued cash and wholesale strength supported hog futures again Thursday, with the expiring April contract rising 37.5 cents to $88.35 and most-active June gaining 25 cents to $105.00. The CME confirmed the preliminary figure for Tuesday’s hog index quote at $85.15, up 23 cents from Monday.

— The detection of avian influenza in dairy cows has spooked cattle markets on fears it will hurt consumer demand for beef or restrict exports, analysts say. Speaking of beef, a grocery list of common items that cost $100 in 2019 would today set you back 36.5% more, a WSJ analysis (link) of NielsenIQ data found.

— Quotes of note:

- More than half a dozen Federal Reserve policymakers gave public remarks Thursday…. A few of them:

Federal Reserve Bank of Minneapolis President Neel Kashkari suggested that interest-rate cuts may not be necessary in the current year if progress on inflation stalls, particularly if the economy maintains its robustness. He mentioned that he had initially considered two rate cuts in March if inflation trends continued toward the Fed's 2% target. However, if inflation remains stagnant, Kashkari questioned the necessity of those rate cuts. Kashkari expressed concern over the inflation readings for January and February, indicating the need for more significant progress on prices to be confident that they are moving towards the Fed's target before considering reducing borrowing costs. He stressed the importance of using inflation data as a guide for interest-rate decisions. Although Kashkari does not have a vote on monetary policy this year, he previously discussed the possibility of not needing rate cuts at an event last month. He highlighted the attractiveness of a scenario where employment is high, businesses are thriving, and inflation is decreasing. The remarks were made during a virtual event hosted by Pensions & Investments and broadcast on LinkedIn.

Philadelphia Fed President Patrick Harker said that even though the economy has been resilient and the labor market remains strong, inflation is “still too high.”

Cleveland Fed President Loretta Mester suggested that the central bank could be close to gaining the confidence it needs to start lowering interest rates later this year, but that she wants to see a couple more months’ worth of data first.

Richmond Fed President Thomas Barkin said it’s “smart” for the central bank to take time to gain greater clarity about the inflation path before lowering rates. He told the Home Building Association of Richmond that the economy is cooling, and said the full impact of higher rates is still coming. “No one wants inflation to re-emerge,” and the strong labor market means there’s time before starting the process of “toggling rates down.”

- The European Central Bank (ECB) is expected to maintain interest rates at the upcoming April 11 meeting and retain its current guidance, according to Jussi Hiljanen, chief strategist for USD and EUR rates at SEB Research. The ECB is likely to affirm its intention for a first interest-rate cut in June. While acknowledging progress toward the inflation target, the central bank will emphasize the need for further evidence of a sustained disinflationary trend. During the press conference, President Christine Lagarde may mention that a rate cut was deliberated but that the Governing Council unanimously opted to keep policy rates unchanged, awaiting additional information on wage negotiations and confidence in the continued disinflationary trajectory.

— Job growth totaled 303,000 in March, much better than expected; unemployment at 3.8%. In March 2024, the U.S. economy experienced a significant increase in job additions, with a notable gain of 303,000 jobs, marking the highest figure in the past ten months. This surpasses the downwardly revised job additions of 270,000 in February, as well as expectations of 200,000 forecasted for March. Last month’s gain is now substantially above the previous 12-month average of 231,000 jobs. Key sectors contributing to this growth include healthcare, government, and construction. The biggest categories of job gains were health care (up 81,300 jobs) and government (up 71,000). It was the 39th straight month of job growth.

Additionally, revisions to January's data revealed an upward adjustment, resulting in a combined increase of 22,000 jobs for January and February compared to previous reports. This suggests that employment trends have been more robust than initially indicated.

Of note: The leisure and hospitality industry returned to its employment level in February 2020, and now sits at about 16.9 million jobs.

These employment gains continue to outperform historical averages and are exceeding the estimated 70,000 to 100,000 jobs needed monthly to accommodate the expanding working-age population.

Restaurateurs say it is finally becoming easier to find employees, after years of worker shortages, relieving the pressure to raise wages. A major pickup in immigration has also helped fill many long-standing openings, with 3.3 million immigrants arriving in 2023, according to the Congressional Budget Office.

The unemployment rate moved to 3.8% last month, equaling estimates of 3.8% and dipping from February’s 3.9%, extending the longest streak of sub-4% unemployment in six decades. The Black unemployment rate rose 0.8 percentage points to 6.4%, the highest since August 2022.

Hourly earnings rose 4.1% from March 2023 to last month, in line with forecasts of 4.1% (average hourly earnings rose 0.3% in March). Wage growth remains steadily above inflation — the most commonly cited inflation measures checked in last month at 2.5% and 3.2% — allowing Americans to regain some of the spending power lost during the worst inflationary period since the early 1980s

The labor force participation rate rose by 0.2 percentage points to 62.7%.

Bottom line: These figures indicate a positive momentum in the labor market and reflect a strengthening of the economy in terms of job creation and expansion.

Market impact: “Investors are on edge [that] the Fed may delay rate cuts from June until later in the summer (or late in 2024) if we get another hot employment report,” Sevens Report founder Tom Essaye explained ahead of the release. The strong hiring reflected in today’s report dims Fed rate-cut hopes. After the March jobs report, markets are pricing in 57% odds of a rate cut by the June 12 Fed meeting, down from 64% odds before the latest data, according to CME Group's FedWatch page. Odds of a rate cut by the July 31 meeting stood at 75%, down from 80%. For all of 2024, markets are pricing in a year-end Fed funds rate of 4.71%, up from 4.66% ahead of the jobs report. That builds in 57% odds of at least three quarter-point rate cuts.

— A Bloomberg assessment recalls that President Biden likes to say he has created 800,000 manufacturing jobs since taking office in January 2021. “And it is true that by February of this year 776,000 more people were working in U.S. factories. An industrial policy-fueled factory-investment boom should also mean many more such gains in the years to come. But the bulk of that addition was simply part of a bounce back from the 2020 pandemic recession. In the 16 months since October 2022, the US economy actually has only added 34,000 manufacturing jobs. In the month of February, factory payrolls actually dropped — by 5,000.”

There’s also a politically important soft spot in Biden’s manufacturing pitch, as noted in a Bloomberg Big Take item: In three key industrial swing states (Michigan, Pennsylvania, and Wisconsin) a collective 39,000 fewer people are working in manufacturing than five years ago.

Meanwhile, Trump likes to proclaim that his trade wars and tax cuts fueled his own manufacturing renaissance. The pandemic shock put an enormous dent in that, however, and over his four years in office the U.S. actually lost a net 75,000 manufacturing jobs. Says Bloomberg: “Even if you strip out the 2020 pandemic year, the picture isn’t as rosy as Trump or his supporters portray. Manufacturing employment under Trump peaked at 12.8 million in January of 2019, more than a year before the pandemic hit, and 43,000 factory jobs were lost in the 12 months after that peak.”

— In February, a rise in agricultural exports helped narrow the monthly trade deficit in the U.S. Agricultural exports increased to $15.72 billion, up by 5.5% from January, while agricultural imports decreased to $16.93 billion, down by 3% from January. This resulted in a trade deficit of $1.21 billion for the month, more than halving from January's $2.54 billion deficit.

In fiscal year (FY) 2024, cumulative agricultural exports amounted to $78.86 billion, with imports totaling $82.93 billion, resulting in a deficit of $4.07 billion.

USDA forecasts agricultural exports to reach $170.5 billion in FY 2024, with imports hitting a record $201 billion, leading to a trade gap of $30.5 billion. To meet USDA's export forecast, agricultural exports would need to average $13.09 billion over the next seven months, similar to the March-September 2023 period. Agricultural imports, averaging $16.87 billion over the next seven months, would need to meet USDA's import forecast, comparable to the final seven months of FY 2023.

If USDA's forecasts materialize, the sector will see monthly trade shortfalls averaging $3.78 billion. FY 2023 witnessed four consecutive months of agricultural trade deficits exceeding $3 billion, with August marking a record deficit of $3.62 billion. The only monthly trade surplus in FY 2024 occurred in November, totaling $99 million.

Of note: With agricultural imports typically peaking and export values typically declining, future trade flows will be influenced by the value of the U.S. dollar in the coming months.

— USDA's NASS unveils changes to livestock reports based on five-year review. USDA's National Agricultural Statistics Service (NASS) announced it plans to make several changes in the number of states where it will report data in the January Cattle Inventory, December Hogs & Pigs, quarterly Milk Production, monthly Cattle on Feed, weekly Broiler Hatchery, and monthly Chickens and Eggs reports (link). Summary of those changes:

- January Cattle Inventory: Reduce the number of published states to 31 from the current 50. NASS will still publish all cattle and calves inventory, all cows inventory, and calf crop for the 19 states (Alaska, Connecticut, Delaware, Hawaii, Indiana, Louisiana, Maine, Maryland, Massachusetts, Mississippi, Nevada, New Hampshire, New Jersey, North Carolina, Rhode Island, South Carolina, Utah, Vermont, and West Virginia).

- December Hogs & Pigs: Reduce the number of published states from 50 to 16. The 16 states are Colorado, Illinois, Indiana, Iowa, Kansas, Kentucky, Michigan, Minnesota, Missouri, Nebraska, North Carolina, Ohio, Oklahoma, Pennsylvania, South Dakota, and Texas. The 34 non-published states will be accounted for in Other States.

- Quarterly Milk Production: Reduce the published states from 50 to 33. The 17 non-published states will be Alabama, Alaska, Arkansas, Connecticut, Delaware, Hawaii, Louisiana, Massachusetts, Mississippi, Montana, New Hampshire, New Jersey, North Dakota, Rhode Island, South Carolina, West Virginia, Wyoming. Those states will be accounted for in Other States.

- Cattle on Feed: Minnesota will be removed as a published state and will be accounted for in Other States.

- Broiler Hatchery: Florida and Louisiana are to be removed from the published states in the weekly report, accounting for them in Other States.

- Chickens & Eggs: Maryland, South Dakota, and Virginia would be removed from the monthly report, and they will be accounted for in Other States. Louisiana, Maryland, Massachusetts, Montana, South Dakota, Virginia, and West Virginia would be removed from a published state in the annual Chickens and Eggs report and accounted for with Other States.

Market perspectives:

— Outside markets: The U.S. dollar index was stronger, but the euro was slightly firmer against the greenback. The yield on the 10-year U.S. Treasury note rose, trading around 4.33%, with a mixed tone in global government bond yields. Crude oil futures were slightly higher, with U.S. crude around $86.65 per barrel and Brent around $90.80 per barrel. Gold futures were higher while silver saw losses, with gold around $2,311 per troy ounce and silver around $26.79 per troy ounce.

— The global benchmark oil price, Brent crude, surged past $90 a barrel for the first time since October due to escalating tensions in the Middle East and existing tight market conditions. This increase is attributed to concerns over potential retaliation from Iran following a suspected Israeli attack on its consulate in Damascus. Throughout the year, oil prices have been steadily rising due to strong economic indicators from major economies like the U.S. and China, indicating increased global demand. Additionally, supply constraints from the OPEC+ alliance, led by Saudi Arabia, have further tightened the market.

The recent surge in oil prices has surpassed earlier forecasts, with prices reaching levels beyond the projected $83 per barrel for this quarter. The breakthrough past the $90 mark signifies a significant bullish signal for traders, prompting increased buying activity. The ongoing geopolitical tensions and optimistic demand outlooks have propelled the rally in oil prices, posing challenges for central banks aiming to control inflation. The U.S. Federal Reserve, especially, has expressed concerns about rising energy prices and their impact on inflation.

JPMorgan Chase forecast last week that oil would climb above $100 by September. And, in a bad sign for motorists, gasoline prices in the U.S. have climbed 6% in the past month just ahead of the North American summer driving season. “If we get a direct conflict between Israel and Iran, that’s something that will likely restrict the supply of oil coming from the Middle East,” Matt Maley, an analyst at Miller Tabak + Co., told Bloomberg.

Meanwhile, the U.S. Department of Energy has canceled plans to purchase oil for replenishing the nation's emergency crude stockpile in response to the escalating prices. The Strategic Petroleum Reserve had been tapped in previous years to address supply shortages caused by events like Russia's invasion of Ukraine. Rising crude prices have also led to higher gasoline prices ahead of the summer driving season, raising concerns in the White House, especially with the presidential election approaching Nov. 5. The U.S. has even intervened diplomatically, urging Ukraine to refrain from targeting Russian oil refineries out of fear that such actions could further fuel the oil price rally.

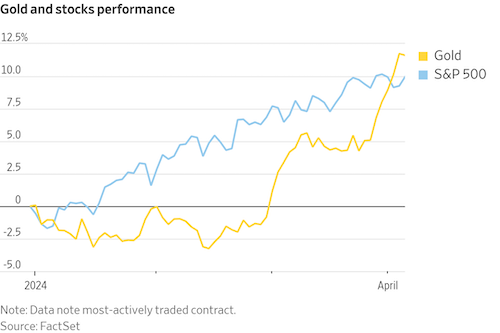

— Gold is now performing better than the S&P 500. Says the Sevens Report: “Our take is that gold initially broke out to new highs thanks to the dual tailwinds of a rapidly declining dollar in Q4 ’23 and the near-100-basis-point drop in real interest rates between October and January. Since early 2024, the dollar has stabilized, and real rates have recovered so neither is still supporting gold. Inflation expectations, however, have moved meaningfully higher, up about 32 basis points to 2.44% since the end of 2023. So, what could cause a pullback? If we see any combination of the following: 1) Inflation expectations stop rising, 2) The dollar breaks out to new highs, and/or 3) Real interest rates move beyond 2% and steadily advance, the gold rally would likely be, at least temporarily, derailed… When gold trends, it trends well. And the latest new highs offer fresh evidence that supports the bull case for gold. Within gold trends, reactionary pullbacks are com-mon. Those are not ideal for portfolio volatility; however, they do offer good opportunities to get into or add to long positions.”

— Biomass-based diesel industry surges as used cooking oil imports exceed predictions, sparking regulatory concerns. American Soybean Assn. (ASA) chief economist Dr. Scott Gerlt, in an article (link), notes the domestic biomass-based diesel industry, encompassing biodiesel and renewable diesel, has experienced significant growth, with capacity increasing from 3.3 billion gallons in 2021 to 5.9 billion gallons by the end of 2023. This growth has been fueled by various feedstocks, including soybean oil, other vegetable oils, used cooking oil (UCO), and animal fats. Importantly, Gerlt says, the consumption of these feedstocks for biofuels has increased, with used cooking oil imports surpassing expectations, particularly from China.

Used cooking oil holds advantages in biofuel programs due to its waste product status, especially in California where it receives a low carbon intensity score under the Low Carbon Fuel Standard. This makes biofuels produced from UCO more valuable, along with other waste feedstocks like tallow and yellow grease.

The increase in used cooking oil imports has implications for the federal blending obligations set by the Environmental Protection Agency (EPA). While renewable diesel consumption is primarily in California, the EPA sets national blending levels based on assumed feedstock availability. Import levels exceeding EPA expectations displace domestic feedstocks, affecting the overall biofuel landscape.

The surge in UCO imports from China in 2023 coincided with concerns raised by Germany regarding biofuel imports from China labeled as made from waste oils, Gerlt observes. European imports of Chinese UCO declined while U.S. imports increased substantially, likely due to differing regulatory scrutiny.

Economic incentives, including credits under California's LCFS, have driven the demand for UCO imports, leading to potential mislabeling concerns, says Gerlt. While EPA requires chain of custody data for UCO, enforcement actions occur after Renewable Identification Numbers (RINs) are generated.

Bottom line: Gerlt says that while the biofuel sector is expanding, imports, particularly of UCO, play a significant role, influenced by regulatory incentives. Monitoring of market behaviors and regulatory oversight, he stresses, is essential to ensure transparency and prevent displacement of domestic feedstocks. He says “EPA assumed that in 2024 renewable diesel imports plus renewable diesel produced from imported feedstocks would drop from 649 million gallons to 166 million gallons. This is further assumed to drop to zero in 2025. If imports remain at their current levels, over 1 billion gallons of biofuels that EPA assumed could be made from domestic feedstocks will instead be produced from foreign feedstocks. The agency assumed the domestic feedstocks came largely from growth in soybean crushing, which is based upon industry expansion to supply soybean oil to renewable diesel plants.”

Of note: Tax credits for biomass-based diesel change in 2025 and will have some effect on this. The Blenders Tax Credit ends in 2025 and the Producers Tax Credit (45Z) starts. “Imported BBD is no longer eligible for tax credits, so renewable diesel imports will likely fall. However, the PTC amounts are dependent upon carbon intensity scores which will give an even stronger incentive to import UCO,” Gerlt concludes.

— Ag trade update: Egypt purchased 250,000 MT of raw sugar from unspecified origins.

— The forecast for the upcoming Atlantic hurricane season predicts an "extremely active" season with nearly two dozen tropical storms, including 11 hurricanes, posing heightened threats to the U.S. coastline. This prediction from hurricane researchers at Colorado State University is based on factors such as record ocean warmth and atmospheric patterns conducive to tropical cyclones. The researchers express high confidence in their forecast, attributing it to the extreme sea surface temperatures across the Atlantic basin. Historically, an average of 14 tropical cyclones form each year, but recent seasons have seen higher activity. The main drivers for this year's expected activity are warm Atlantic surface waters and the potential development of a La Niña climate pattern, both of which provide favorable conditions for storm formation. While warm water alone doesn't guarantee hurricanes, it significantly contributes to their likelihood. The heightened risks of landfalling storms in the U.S., particularly along the East Coast, are emphasized, along with the increased risks for islands and coastal areas due to exceptionally warm waters in the Gulf of Mexico and Caribbean. The forecasters urge preparations for potentially violent storms, acknowledging that while forecasts are improving, there's still some uncertainty at this stage.

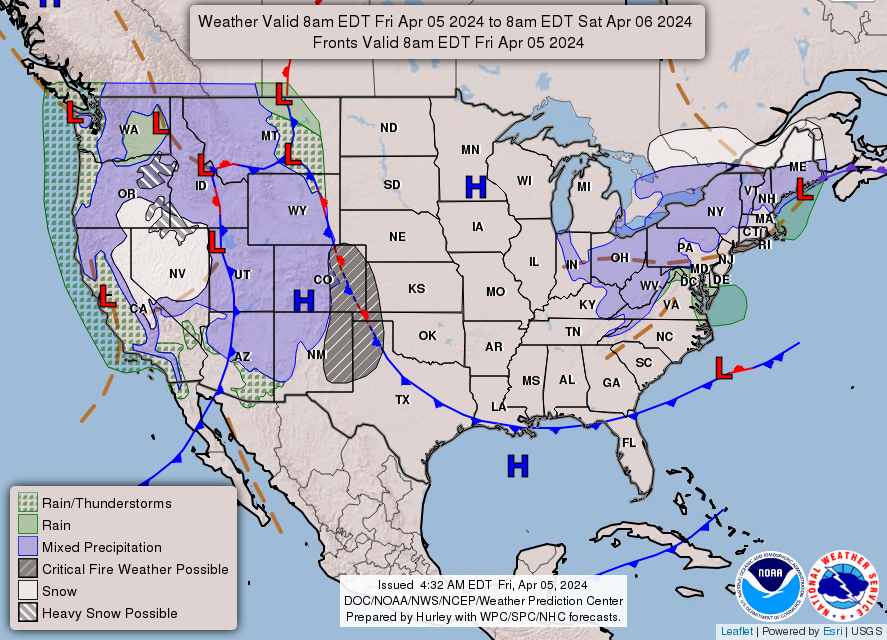

— NWS weather outlook: Wet snow lingers over northern New England into Saturday... ...Widespread mountain snow moves across the interior western U.S... ...High Winds expected to impact the Four Corners today, spreading across the Rockies and High Plains on Saturday, reaching into the central Plains by Sunday... ...Severe thunderstorms possible over the central Plains later on Saturday into early Sunday... ...Critical Fire Risk for central/southern High Plains through this weekend.

Items in Pro Farmer's First Thing Today include:

• Wheat leads overnight price gains

• French wheat crop ratings slip

• Yellen focuses on China’s excess industrial capacity

|

BALTIMORE BRIDGE COLLAPSE |

— U.S. Corps of Engineers announced plans to reopen the Port of Baltimore, which was closed due to wreckage from the cargo ship Dali and a section of the Francis Scott Key Bridge collapse. They aim to have limited access restored by the end of April and full shipping capabilities by the end of May. Weather conditions and complexities in the wreckage may affect this timeline.

Salvage crews are diligently working to remove containers from the Dali and debris from the bridge collapse. Safety is a top priority, with divers assessing the situation after each removal. Maryland State Police divers are on standby for any recovery efforts related to missing workers.

In terms of relief efforts, the Small Business Administration is assisting affected businesses with loans and deferrals on payments. Additionally, the Maryland government is providing financial aid to impacted workers and families of victims. The mayor of Baltimore emphasized the importance of supporting families directly affected by the tragedy.

— President Joe Biden will visit Baltimore today, where he is scheduled to meet with some of the relatives of the six construction workers who died in the collapse of the Francis Scott Key Bridge. The White House previously said Biden would be meeting with local officials and viewing the wreckage of the bridge, which collapsed last week after a massive cargo ship hit one of its support pillars.

— Congress should fully repair costs to Baltimore’s collapsed bridge, the Biden administration urged in a letter to (link) key lawmakers. Meanwhile, preliminary findings of a probe into the collapse are set for release by the National Transportation Safety Board within days

— Eleven cargo ships, including four crucial for national defense, are stuck behind the wreckage of the Francis Scott Key Bridge in the Port of Baltimore. The four ships are part of the Ready Reserve Force, meant to rapidly supply American troops globally. Naval experts express concern, noting the reduced fleet size and reliance on civilian vessels for emergencies like Desert Storm. Clean-up efforts after the bridge collapse are ongoing but hampered by stormy conditions. Temporary channels only accommodate smaller vessels, leaving larger ships stranded. The Maritime Administration plans to expand the Ready Reserve Force with updated ships. Other vessels stuck in the port face financial losses. Additionally, six bulk ships are anchored south of the Bay Bridge.

— The Baltimore bridge collapse represents a multifaceted challenge due to the presence of a high-pressure natural gas pipeline running beneath it, compounded by the massive cargo ship's impact. The pipeline, spanning the shipping channel, posed an imminent danger during the bridge collapse. Efforts to mitigate the risk included lowering the pipeline's pressure and purging it of gas over six days. The pipeline's location beneath the ship adds complexity to salvage operations, as its integrity must be maintained. Additionally, other infrastructure, such as an inactive water main and telephone line, complicates the situation.

Challenges ahead. Despite the danger being mitigated and salvage efforts progressing, the presence of these underground utilities poses ongoing challenges. Salvors must carefully clear the wreckage without damaging the infrastructure below, including the gas pipeline. The depth and soil density of the pipeline are crucial factors to consider, especially as salvors work to refloat the grounded ship. The potential for damaging the pipeline adds complexity to the salvage operation, necessitating a meticulous approach to ensure safety and prevent further environmental and economic repercussions.

|

CONGRESS |

— House Ways and Means Committee plans to address future tax policy in a hearing on April 11, as announced by committee Chair Jason Smith (R-Mo.). With several provisions of the 2017 GOP-led tax law set to expire in 2025, lawmakers have been discussing priorities for the upcoming tax fight. Republicans are considering forming tax policy working groups to guide their approach to different aspects of the tax code, although the exact categories for each group are yet to be determined. The formation of these groups aims to help members understand key issues and establish priorities, particularly considering the turnover in committee membership since the passage of the 2017 law. In the past, the committee has utilized bipartisan working groups to focus on various topics, including energy, international tax, and pass-through entities.

— Senate Republicans are poised to block a $78 billion tax-cut package, betting on winning the majority in November to pursue larger business breaks. They aim to deny President Biden an election-year win, opposing legislation that includes child and business tax breaks. Although the bill garnered bipartisan support in the House and White House backing, Senate Republican leaders Mitch McConnell (R-Ky.) and John Thune (R-S.D.) now oppose it. Thune, vying for leadership, doesn't want to clash with key committee leader Crapo, who seeks changes to the bill, including stricter requirements for child tax credits. Democrats reject these alterations, which were previously agreed upon. The package would reinstate tax breaks for businesses and enhance child tax credits for working parents, but Senate GOP opposition risks its passage.

|

ISRAEL/HAMAS CONFLICT |

— President Biden called Israeli Prime Minister Benjamin Netanyahu and called the humanitarian situation in Gaza “unacceptable” and pushed for an immediate ceasefire. It was America’s sternest rebuke of Israel in decades. Pressure on Israel has mounted since it killed seven aid workers in an air strike on Monday.

— Israel to open new border crossing in northern Gaza to increase aid delivery. Israel’s war cabinet approved the opening of a key border crossing in northern Gaza as pressure has mounted for the nation to get more critical humanitarian aid access to struggling Palestinians.

|

RUSSIA/UKRAINE |

— Two RIF Russian grain cargoes receive phytosanitary certificates. Two grain cargoes loaded by Russia’s RIF have received phytosanitary certificates, a company source told Reuters. One of the ships, loaded with 65,000 MT of wheat for Egypt’s state grain buyer, has been released from a port in Russia after being detained amid a dispute between Russian authorities and an exporter, according to the company and two sources with direct knowledge of the matter. The other cargo of 40,000 MT of grain, is not destined for Egypt and remains at a Russian port.

|

CHINA UPDATE |

— Argentine President Milei's shift on China: Balancing ideology and economic pragmatism. An in-depth Bloomberg article (link) delves into the evolving stance of Argentine President Javier Milei regarding trade relations with China and its implications for Argentina's economy and foreign policy. Eight months ago, Milei expressed strong reservations about ties with China, likening it to dealing with an assassin. However, he now acknowledges the importance of China in Argentina's economy, stating that trade relations remain unchanged and emphasizing libertarian principles that allow individuals to engage in business with China if they wish.

China's significant investments span various sectors of Argentina's economy, including commodities, energy, banking, and infrastructure projects. These investments have become crucial to Argentina's economic stability, particularly considering Milei's plans to deregulate the economy. Milei's pragmatic shift is evident in his recognition of the necessity of maintaining ties with China, despite his earlier criticisms.

Furthermore, Milei's government is attempting to attract investments from other nations while relying on China's support to stabilize the economy and potentially transition away from the peso. The $18 billion currency swap with China plays a critical role in Argentina's economic stability, though risks of peso devaluation and hyperinflation persist.

— Brookings: How will Biden and Trump tackle trade with China? Based on available data, Biden’s approach has delivered greater relative gains. Trump’s term, by contrast, was defined by a trade war that came at a heavy cost to the American economy. Link for details.

|

LIVESTOCK, NUTRITION & FOOD INDUSTRY |

— FAO food price index ends prolonged slide in March. The UN Food and Agriculture Organization global food price index rose 1.1% in March, ending a seven-month slide, as increases in the prices for vegoils, dairy products and meat slightly more than offset decreases for sugar and cereal grains. The March index was still down 7.7% from last year. Compared to year-ago, prices declined 1.5% for meat, 8.2% for dairy, 20.1% for cereal grains and 0.9% for vegoils, while sugar prices rose 4.8%.

— New cases of Highly Pathogenic Avian Influenza (HPAI) were confirmed in Ohio, bringing the total number of states affected to six. USDA’s Animal and Plant Health Inspection Service (APHIS) confirmed the presence of HPAI in a herd in Ohio that received cattle from a dairy herd in Texas on March 8. Additional cases have also been reported in New Mexico and Kansas. USDA lists the confirmation dates for Ohio as April 2 and for Kansas, New Mexico, and Idaho as April 1. Unlike its reporting on poultry, USDA has not provided specific numbers of affected animals. Meanwhile, APHIS has officially confirmed new cases of HPAI in poultry, including layer flocks in Michigan and Texas. The Michigan case involves 1.93 million birds, while the Texas case involves 1.89 million birds. This brings the total number of affected birds to 3.85 million over the past three days, spanning three commercial flocks and seven backyard flocks.

Of note: Texas Agriculture Commissioner Sid Miller said in an AgriTalk interview that he did not expect HPAI to disrupt beef production. Texas is the No. 1 cattle state, with 12 million head, or roughly one of every seven head in the nation. “The cattle that get it are the older lactating cows, and we don’t have those in the feedlot,” said Miller. “I think we’re OK, but we’re certainly going to research that.”

— Hype or legit concern? Bird flu pandemic could be ‘100 times worse’ than Covid, scientists warn. Link to this article in the New York Post and decide whether the information is on target or hype.

— Iowa House passes food labeling bill amid controversy over egg substitute purchase restrictions. The Iowa House recently passed a bipartisan food labeling bill aimed at preventing imitation meat products from being misleadingly labeled as meat. However, controversy arose when an amendment was added to the bill restricting the purchase of egg substitutes through food assistance programs. The bill, Senate File 2391, passed with a 60-34 vote and imposes fines on businesses mislabeling non-meat products. It specifically targets substitute meat products made from insects, lab-grown meat, and plants, requiring labels to include terms like "fake" or "vegetarian" if they don't contain traditional meat.

The amendment caused opposition from Democrats. It not only added labeling requirements and fines for misbranding fabricated egg products as eggs but also imposed purchasing restrictions on egg substitutes for those using Supplemental Nutrition Assistance Program (SNAP) or Special Supplemental Nutrition Program for Women, Infants, and Children (WIC) benefits.

The bill, with the amendment, now returns to the Senate for further consideration.

|

POLITICS & ELECTIONS |

— Centrist group No Labels announced its decision not to field a ticket in the 2024 presidential election due to a lack of candidates deemed capable of winning the White House. Despite having obtained ballot access in 21 states and potential pathways in others, the group struggled to recruit candidates of significant stature. This difficulty was compounded by opposition from Democrats who feared such an effort might aid the re-election of former President Donald Trump. The decision comes shortly after the passing of one of the group's co-chairmen, former Senator Joseph Lieberman. News of No Labels' withdrawal from the presidential race was first reported by the Wall Street Journal.

— Bill Clinton to publish a memoir about life after the White House. Former President Bill Clinton said he will release a memoir about the "twenty-three-plus years" of his life since leaving the White House.

— Charlie Cook: For Democrats, securing a "firewall" to safeguard their interests hinges on winning back control of the House of Representatives. Cook notes that while in past presidential elections, the term "firewall" referred to crucial states necessary for White House victory, President Biden's key states for success include Michigan, Pennsylvania, Wisconsin, along with either Nebraska's 2nd Congressional District or Maine's 2nd. However, with Biden facing challenges and the Senate majority likely slipping away from Democrats, Cook believes the House presents the most feasible opportunity for the party to establish a protective barrier.

|

OTHER ITEMS OF NOTE |

— Cotton AWP falls under 70 cents. The Adjusted World Price (AWP) for cotton will be 69.48 cents per pound, effective today (April 5), down from 70.88 cents per pound the prior week and the first time under 70 cents per pound since the week of Feb. 2 when it was 68.04 cents per pound. That still leaves the AWP nearly 17.5 cents per pound above the level that would trigger an LDP. Meanwhile, USDA announced that Special Import Quota #25 will be established April 11 for the import of 31,702 bales of upland cotton, applying to supplies purchased not later than July 9 and entered into the U.S. not later than Oct. 7.

— National Corn Growers Association opposes Corteva's petition for antidumping and countervailing duties on the herbicide 2,4-D from India and China. NCGA President Harold Wolle expressed concerns to the International Trade Commission, stating that imposing tariffs could limit imports, increase prices, and lead to supply shortages. Wolle emphasized that such tariffs would exacerbate economic challenges for farmers, who are already price takers and rely on managing production costs for success. Link to NCGA statement.

Meanwhile, herbicide formulator Drexel Chemical voiced opposition to Corteva's claims of market flooding by imports from India and China. Corteva argues that tariffs are necessary due to pricing disparities affecting their sales and capacity utilization. However, formulators disputed Corteva's assertions, alleging that Corteva has prioritized its own product over supplying formulators, leading to increased reliance on imports

The ITC is expected to release a report on 2,4-D imports by March 22, followed by a vote on whether to affirm domestic production injury and proceed with imposing duties on March 26.

|

KEY LINKS |

WASDE | Crop Production | USDA weekly reports | Crop Progress | Food prices | Farm income | Export Sales weekly | ERP dashboard | California phase-out of gas-powered vehicles | RFS | IRA: Biofuels | IRA: Ag | | Russia/Ukraine war, lessons learned | | SCOTUS on WOTUS | SCOTUS on Prop 12 pork | New farm bill primer | | Gov’t payments to farmers by program | Farmer working capital | USDA Ag Outlook Forum |