EPA Finally Releases RFS Proposals | Mixed Reaction

Employment report | USDA farm income | Rail strike averted | Ag disaster aid for 2022

|

In Today’s Digital Newspaper |

Today's focus is the November jobs report. The data will carry considerable implications for the direction of the economy and Federal Reserve policy. Today’s employment report will reveal how the labor market fared in November amid rising interest rates and high inflation.

EPA put out a lot of pages of proposals for multiyear RFS mandates. We have details and reaction in the Energy section.

USDA updated its farm income forecasts for 2022 and there were significant changes from its prior forecasts even though the supply/demand forecasts didn’t change that much since the last farm income outlook.

As we have noted repeatedly, an ag disaster package for eligible 2022 crops and livestock will likely be part of an omnibus spending package Congress will vote on before they adjourn.

|

MARKET FOCUS |

Equities today: Global stock markets were mostly weaker overnight. U.S. stock indexes are pointed toward slightly lower openings.

U.S. equities yesterday: The Dow fell 0.6%, 194.76 points, to 34.395.01. The Nasdaq Composite gained 0.1%, 14.45 points, to 11,482.45. The S&P 500 was off 0.1%, falling 3.54 points to 4,076.57.

Agriculture markets yesterday:

- Corn: March corn fell 6 1/2 cents to $6.60 1/2, the contract’s lowest close since Nov. 22.

- Soy complex: January soybeans sank 39 3/4 cents to $14.29 3/4, the contract’s lowest close since Nov. 22. January soymeal rose $3.80 to $421.60, the highest since Sept. 22. January soyoil fell 450 points to 67.38 cents, the lowest since Oct. 18.

- Wheat: March SRW wheat fell 12 1/2 cents to $7.83. March HRW wheat dropped 9 1/2 cents to $8.90 1/4. March spring wheat fell 5 cents to $9.38.

- Cotton: March cotton rose 24 points to 84.85 cents, the contract’s highest close since Nov. 17.

- Cattle: February live cattle fell 25 cents to $155.425. January feeder cattle rose 60 cents to $181.075.

- Hogs: February lean hogs surged $3.825 cents to $89.175, the contract’s highest close since Nov. 22.

On tap today:

• U.S. nonfarm payrolls are expected to rise by 200,000 in November and the unemployment rate is forecast to hold steady at 3.7%. (8:30 a.m. ET)

• Baker Hughes rig count is out at 1 p.m. ET.

• CFTC Commitments of Traders report, 3:30 p.m. ET.

• Federal Reserve speakers: Richmond's Thomas Barkin on the labor market at 9:15 a.m. ET, Chicago's Charles Evans on financial regulations at 10:15 a.m. ET, and Mr. Evans at an economic outlook symposium at 1:15 p.m. ET.

Mexico’s minimum wage bump. Mexico plans to raise its minimum wage by 20 percent starting on January 1, 2023, officials said on Thursday. The minimum wage, now 172 Mexican pesos, or $9, will increase to 207 Mexican pesos, or around $10.82.

USDA forecasts for U.S. farm income and expenses raised for 2022. U.S. net farm income in 2022 is now forecast at $160.5 billion, up $19.5 billion from 2021, and up $12.8 billion from USDA’s September outlook, according to the Economic Research Service (ERS). Net cash farm income is now forecast at $187.9 billion for 2022, up $39.4 billion from 2021 and up from a September forecast of $168.5 billion. When adjusted for inflation, net farm income would be the highest since 1973 while net cash farm income would be highest since USDA’s inflation-adjusted series started in 1929.

Nearly all expense categories are forecast to rise in 2022 compared with the previous year, with cash expenses to total $412.1 billion versus $408.5 billion in September and $345.4 billion in 2021. The most significant increases are expected in fertilizer-lime-soil conditioner costs, forecast up $13.9 billion in 2022 versus 2021, putting them at $43.4 billion. Feed expenses are seen hitting $76.6 billion, up $11.3 billion in 2022 versus 2021, while interest expenses, not surprisingly, are to rise $8 billion, hitting $27.4 billion. On a percentage basis, fertilizer-lime-soil conditioner costs are up 47%, feed expenses up 17.4%, interest expenses up 41% and fuel and oil expenses are up 47.4%.

Working capital strong. While farmers are seeing higher expenses, they have built a sizable amount of working capital. USDA forecasts working capital on farms at $134.5 billion, up from $126.5 billion in 2021 and the recent low point of $65.2 billion in 2016. The infusion of payments from the government has contributed to the “war chest” that farmers must work with as they deal with higher input costs. The increase in working capital is 4.7% in nominal dollars, but when adjusted for inflation, it is down 1.4%. Farm sector equity is expected to increase by $320.8 billion in 2022 to $3.34 trillion, with assets forecast to hit $3.85 trillion, up $348.6 billion. The debt-to-asset ratio is put at 13.05 by ERS for 2022, down from 13.56 in 2021, and the lowest since it was at 12.99 in 2017. Similarly, the debt-to-equity ratio, at 15.01, is down from 15.68 in 2021 and the lowest since it was at 14.93 in 2017.

Lower government payments vs 2021. The income component of US government payments to farmers is one area that declined in 2022 compared with 2021. Direct Government payments are forecast to fall by $9.4 billion (36.3%) from 2021 to $16.5 billion in 2022. But that is still above USDA’s September outlook that those payments would be $13 billion. “This decrease is expected largely because of lower supplemental and ad hoc disaster assistance for Covid-19 relief in 2022 relative to 2021,” USDA observed. The government payment forecast for 2022 is also well below 2020 when payments from the government hit $45.6 billion, so the 2022 result is down 64% in just two years.

More supplemental ad hoc disaster payments and other assistance helped to boost the government payment total versus the September outlook. USDA sees supplemental and ad hoc assistance at $11.9 billion, which includes $1.2 billion in pandemic assistance and $10.69 billion in other supplemental and ad hoc disaster payments.

Payments under the traditional safety net programs are also seen being down from 2021 levels. Payments received in 2022 under the Price Loss Coverage (PLC) program are forecast at $248.6 million, down from $2.1 billion in 2021. Payments under the Agriculture Risk Coverage (ARC) are seen at $105 million, down from $117.5 million in 2021. The Dairy Margin Coverage program was initially forecast to bring in more money in 2022 than it paid out, but that has shifted—USDA now sees $85.7 million paid to producers versus a prior outlook that the program bring in $10 million more than was paid out.

USDA also forecasts that $3.1 million will have been paid out in loan deficiency payments in 2022, down from $7.1 million in 2021, with no marketing loan gains paid after just $36,000 were paid in 2021.

Market perspectives:

• Outside markets: The U.S. dollar index is lower and hit a 3.5-month low overnight. Meantime, the yield on the benchmark U.S. 10-year Treasury note is presently 3.515%.Nymex crude oil prices are near steady and trading around $81.00 a barrel.

• The average cost of regular unleaded gasoline fell to $3.45 a gallon on Thursday, according to OPIS, an energy-data and analytics provider. That is among the lowest levels since Russia’s invasion of Ukraine in February and a more than 30% drop from a record above $5 in June, according to OPIS.

• World food prices ease for eighth straight month. The U.N. Food and Agriculture Organization (FAO) global food price index ticked down 0.2 point in November – the eighth straight monthly decline – though it was 0.4 point (0.3%) above year-ago. Declines in cereal grains, dairy and meat slightly more than offset increases in vegetable oils and sugar. Compared to year-ago, prices were up 4.1% for meat, 9.1% for dairy and 6.4% for cereal grains, while vegoils dropped 16.2% and sugar declined 4.9%.

• FAO cuts global cereal grain production forecast. FAO’s world cereal grain production forecast for 2022-23 was cut 7.2 MMT from last month to 2.756 billion metric tons, due mainly to smaller corn production. Cereal grin production is now expected to fall 57 MMT (2.0%) from 2021-22.

• Mexico, U.S. trade officials discuss corn exports, energy policy. U.S. Trade Representative Katherine Tai met Mexican Economy Minister Raquel Buenrostro and stressed the importance of avoiding any disruption in U.S. corn exports to Mexico along with Mexico’s energy policy. The Mexican economy ministry has invited Tai’s team to hold consultations in the coming days in Mexico City. Buenrostro proposed establishing working groups, which would meet during December and early January to discuss the different aspects of the energy consultations.

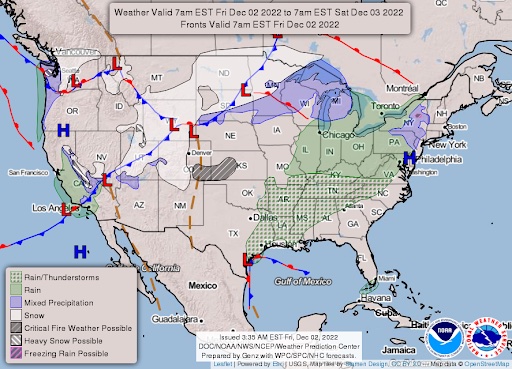

• NWS weather: A quick round of mountain snow will move across the northern and central Rockies followed by the northern Plains today... ...A slow-moving low pressure system will bring lingering rain along coastal Pacific Northwest before heavy precipitation reaches into California on Saturday... ...Polar air surges southward into the central U.S. as mild and wet weather surges up the East Coast on Saturday.

|

RUSSIA/UKRAINE |

— Hospitalized U.S. hostage. Paul Whelan, a former U.S. Marine who has been detained in Russia since 2018, has reportedly been hospitalized, his family said. Whelan now has not been in contact with his family for a week, and has missed a planned phone call, which they said was unusual. Washington has previously suggested conducting a prisoner swap of Whelan and U.S. basketball star Brittney Griner for Viktor Bout, a Russian arms dealer. “We are deeply concerned about the lack of information and the lack of contact from Paul, and we’re working on this really as hard as we can through diplomatic channels,” U.S. National Security Council spokesperson John Kirby said.

|

POLICY UPDATE |

— As expected, a big omnibus spending package will include disaster aid for eligible 2022 crops and livestock. And it looks like the language will direct USDA a bit more than usual because some farm-state lawmakers, and farmers, do not like how USDA may implement Phase 2 of the Emergency Relief Program (ERP).

|

CHINA UPDATE |

— China gives major signal it may adjust its stringent zero-Covid policy that sparked a wave of protests. The top official in charge of China’s Covid response told health officials Wednesday that the country faced a “new stage and mission” in pandemic controls. “With the decreasing toxicity of the Omicron variant, the increasing vaccination rate and the accumulating experience of outbreak control and prevention, China’s pandemic containment faces a new stage and mission,” Vice Premier Sun Chunlan said Wednesday, according to state news agency Xinhua. Her comments came a day after a separate body of top health officials pledged to rectify some approaches to Covid control and said local governments should “respond to and resolve the reasonable demands of the masses” in a timely manner. Case numbers in the past week have hovered around record highs, with more than 34,000 new infections reported Thursday — posing a steep challenge to efforts to return them to a low level. As of Nov. 11, 40% of China’s over-80 population had received a booster shot, according to state media, while around two-thirds had received two doses. Meanwhile, several cities have made revisions to their policies, largely around testing and quarantine rules, while some have relaxed lockdown measures.

|

ENERGY & CLIMATE CHANGE |

— EPA’s RFS proposals would bring major changes to the U.S. biofuel mandate, including a plan to encourage use of renewable natural gas to power electric vehicles. The proposals could prompt an overhaul that shifts the program's focus away from gasoline, diesel and other liquid fuels to a broader plan aimed at decarbonizing transportation. EPA said it will seek comment "on this new component of the RFS program that would tie electricity generation from renewable biomass into the program for the first time."

EPA also wants public comment on how its plan would affect the "continued viability of domestic oil refining assets, including merchant refiners" with limited blending facilities that cannot easily generate compliance credits (RINS), as well as "how best to support novel fuels like sustainable aviation fuels and clean hydrogen, and how to account for the new and updated incentives in the Inflation Reduction Act."

The proposal calls for:

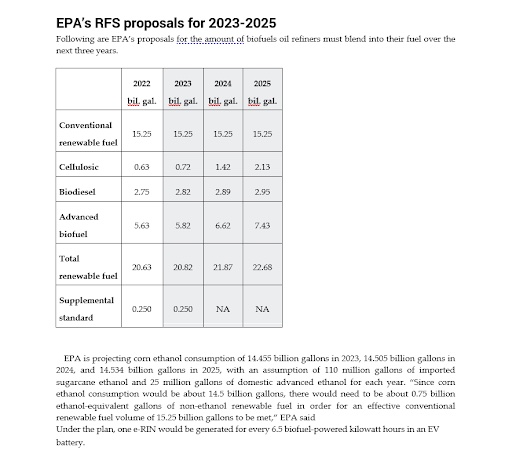

EPA noted that inclusion of supplemental volume requirement results in implied requirement of 15.25 billion gallons of conventional biofuel for 2022 and 2023, and is an “appropriate candidate volume” for 2024 and 2025.

EPA is projecting corn ethanol consumption of 14.455 billion gallons in 2023, 14.505 billion gallons in 2024, and 14.534 billion gallons in 2025, with an assumption of 110 million gallons of imported sugarcane ethanol and 25 million gallons of domestic advanced ethanol for each year. “Since corn ethanol consumption would be about 14.5 billion gallons, there would need to be about 0.75 billion ethanol-equivalent gallons of non-ethanol renewable fuel in order for an effective conventional renewable fuel volume of 15.25 billion gallons to be met,” EPA said.

With proposed volume requirements of 5.1 billion RINs for 2023, 5.2 billion RINs for 2024 and 5.3 billion RINs for 2025, EPA said that would result in excess RIN supplies of 795 million in 2023, 745 million in 2024 and 716 million in 2025. “This excess non-cellulosic advanced biofuel would make up for the shortfall in corn ethanol, enabling an implied conventional volume of 15.00 billion gallons in 2023 and 15.25 billion gallons in 2024 and 2025 to be met, and also enable the 250-million-gallon supplemental volume to be met,” EPA said.

Regarding renewable diesel, EPA said: “In total over 5 billion gallons of new renewable diesel capacity has been announced, though it is likely that not all these announced projects will be completed, and not all of those that are completed will necessarily produce renewable diesel in the 2023–2025 timeframe addressed by this rule.” The current renewable diesel production capacity was put at 1.5 billion gallons as of February 2022. Looking forward, EPA said that given high costs for renewable diesel plants, the sourcing of feedstocks will be important. “It appears more likely that the announced renewable diesel facilities will not be built if sufficient feedstock to operate these facilities at or near their production capacity cannot be secured,” feedstock to operate these facilities at or near their production capacity cannot be secured,” EPA noted.

As for eRINS, the proposal includes RINs from renewable electricity (eRINs) and how they may work under the RFS. The proposal covers several key areas “including which parties can generate eRINs, prevention of double-counting, and data requirements for valid eRIN generation.” The plans, EPA said, are aimed at providing “clarity on how electricity would be incorporated into the RFS so that the existing RIN-generating pathway can be effectively utilized in a manner that ensures RINs are generated only for qualifying electricity.”

As to who can generate eRINs, EPA is proposing that vehicle original equipment manufacturers are the ones that can generate eRINs “based on the light-duty EVs they sell by establishing contracts with parties that produce electricity from qualifying biogas (renewable electricity generators).” EPA is proposing that eRINs would represent the “quantity of renewable electricity determined to be used by both new and previously sold (legacy) light-duty electric vehicles for transportation, provided that sufficient renewable electricity has been produced and contracted by the OEM.”

Requirements for biogas generators and electricity producers will be set up, EPA said, “but only an OEM would be allowed to generate the eRIN.” However, the value of the eRIN would be expected to be “distributed after its generation amongst multiple parties.”

EPA is:

- proposing to adjust the equivalence value for electricity in the RFS, replacing the current value of 22.6 kilowatt-hours (kWh) with 6 kWh per RIN.

- proposing the eRIN requirements become effective beginning on Jan. 1, 2024, and are seeking comments on “all aspects” of their proposal.

For the 2023–2025 timeframe, EPA expects that commercial scale production of cellulosic biofuel in the U.S. will be limited to electricity and CNG/LNG derived from biogas.

Tracking the biogas through to the use in vehicles is a key, a situation not found relative to ethanol or biodiesel. “For example, once ethanol is denatured, it is reasonably presumed that it will be used as transportation fuel as it has no other practical uses,” EPA stated. “Similarly, once biodiesel meets highway fuel specifications, it is presumed that it will be used as transportation fuel.” For biogas to be transported via pipeline or in some cases used to generate power, it has to be “cleaned up,” as EPA put it, and typically biogas is converted over the renewable natural gas (RNG) and then it can be converted to electricity. When RNG is added to a natural gas pipeline system, EPA noted it is mixed with fossil fuel natural gas. “We are unable to assume that the main use of the RNG will be for transportation because only a small percentage of natural gas used in the United States is used for transportation,” EPA said.

EPA assumes there will be 600 million RINs from renewable electricity in 2024 and 1.2 billion RINs from renewable electricity in 2025.

Meanwhile, the Biden administration approved canola oil for use in making renewable diesel and other biofuels, qualifying fuels blended with the oilseed to meet federal standards, the EPA said on Thursday.

Mixed reaction. Ethanol groups are applauding the EPA announcement while biodiesel and advanced biofuel groups say the numbers don’t reflect the growth in renewable diesel and other products.

The American Soybean Association (ASA) said: “Soybean farmers were heartened by EPA’s 2022 volume target—which included the highest-ever number for total renewable fuels and specifically for biomass-based diesel (BBD) since the renewable fuel standard was created — and were hopeful EPA would stay the course on a rising trajectory. However, the numbers released by EPA show a reversal rather than affirmation of its commitment to BBD. Even more, EPA has proposed halting any growth for advanced biofuels outside of BBD and cellulosic biofuels. The multi-year set rule was intended to provide more certainty for the biofuels industry and encourage investment and innovation. Contrarily, these very insignificant volume increases for 2023-2025 realistically could not only stifle growth but also jeopardize the existing biofuels industry. “America’s farmers have committed to the renewable fuels industry while continuing to provide the feed and food our country and other countries must have. Billions of dollars have gone into building and growing the infrastructure needed to support this industry. And our president has made a clear commitment to mitigating climate change and lowering greenhouse gas emissions — the very tenets of the RFS,” said ASA President Brad Doyle in a release following the announcement. “And, yet, this draft rule slams the brakes on progress being made in biofuels investment and growth. Instead of continuing to support available, low-emission plant-based fuel sources, EPA has changed course and seemingly is ignoring the major investments in and consumer demand for biomass-based diesel and other biofuels that exists right now,” Doyle continued.

Now what? EPA has set Feb. 10 as the comment deadline for the proposed rule. Extensions of comment periods are likely. EPA has set a public hearing on the RFS proposals for Jan. 10, 2023 and has pledged to finalize the rule by June 14, 2023.

Year-round E15. Separately, a bipartisan group of Senators, including Sens. Dick Durbin (D-Ill.) and Deb Fischer (R-Neb.), introduced the Consumer and Fuel Retailer Choice Act to allow the year-round nationwide sale of ethanol blends higher than 10%. Link to text.

— Biden administration wants to halt SPR sales to refill depleted stockpiles. The Biden administration is seeking to stop sales from the Strategic Petroleum Reserve (SPR), mandated by Congress, so it can refill the emergency reserve. The move could impact the release of 147 million barrels of crude oil, Doug MacIntyre, an Energy Department official, told a Senate panel Thursday. Such a plan, which would require congressional approval, could be attached to a must-pass government funding bill that could come together this month.

|

HEALTH UPDATE |

— Summary:

- Global Covid-19 cases at at 644,118,669 with 6,637,952 deaths.

- U.S. case count is at 98,923,209 with 1,081,147 deaths.

- Johns Hopkins University Coronavirus Resource Center says there have been 653,502,647 doses administered, 267,804,921 have received at least one vaccine, or 81.28% of the U.S. population.

|

CONGRESS |

— Senate votes 80-15 to avert rail strike, but nixes inclusion of seven days of paid leave as the amendment by Sen. Bernie Sanders (I-Vt.) failed on vote of 52-43 — 60 votes were needed to have approved the amendment.

— Defense policy bill tied to water resources legislation. The House is on track to vote on a compromise annual defense authorization bill by the middle of next week. The measure will be considered as an amendment to H.R. 7776, the Water Resources Development Act. The Rules Committee on Monday afternoon is scheduled to consider the measure

|

OTHER ITEMS OF NOTE |

— Former President Donald Trump was dealt a major defeat after a federal appeals court on Thursday halted the special master review of documents seized from his Mar-a-Lago estate. The ruling removes a significant obstacle to the Justice Department's investigation into the mishandling of government records from Trump's time in the White House.

— Cotton AWP declines. The Adjusted World Price (AWP) for cotton eased to 73.03 cents per pound, effective today (Dec. 2), down from 74.61 cents per pound the prior week. Meanwhile, USDA said that Special Import Quota #6 will be established Dec. 1 for the import of 46,370 bales of upland cotton, applying to supplies purchased not later than Feb. 28 and entered into the US not later than May 29.

|

KEY LINKS |

WASDE | Crop Production | USDA weekly reports | Crop Progress | Food prices | Farm income | Export Sales weekly | ERP dashboard | California phase-out of gas-powered vehicles | RFS | IRA: Biofuels | IRA: Ag | Student loan forgiveness | Russia/Ukraine war, lessons learned | Election predictions: Split-ticket | Congress to-do list | SCOTUS on WOTUS | SCOTUS on Prop 12 | New farm bill primer | China outlook |