Retail Sales Jumped 0.7% in March, Much Higher than Expected

Biden advises restraint to Israel amid calls for calm as market nerves ease

|

Today’s Digital Newspaper |

MARKET FOCUS

- Retail sales jumped 0.7% in March, much higher than expected

- Biden advises restraint to Israel amid calls for calm, market nerves ease

- Goldman Sachs’ profits rose 28% in the first quarter, far ahead of analysts’ estimates

- Samsung displaced Apple as world’s biggest phonemaker in first quarter of 2024

- Asahi aims for half of beverage sales from zero-alcohol drinks by 2040

- ECB set for June interest rate cut, further reductions hinge on inflation trends

- Gold’s surge triggered by more than inflation, geopolitical tensions & monetary policies

- Metal prices rose after U.S. & UK imposed new sanctions on Russian supplies

- Ag markets today

- USDA daily export sale: 165,000 MT corn to Mexico (details below)

- Ag trade update

- End of Panama's dry season approaching, bringing hope for increased vessel traffic

- India forecasts above-average monsoon rains

- NWS weather outlook

- Pro Farmer First Thing Today items

BALTIMORE BRIDGE COLLAPSE

- FBI opens criminal investigation on container ship

CONGRESS

- Energy Secretary Granholm before Senate panel tomorrow

- Harris decides to maintain role as chair of Appropriations Agriculture Subcommittee

ISRAEL/HAMAS CONFLICT

- Biden advises restraint to Israel amid calls for calm, market nerves ease

RUSSIA & UKRAINE

- Ukraine’s oilseed production expected to fall around 3%

- UN nuclear watchdog welcomes cold shutdown of Zaporizhzhia reactors

POLICY

- Rural discontent fuels far-right surge in European politics

CHINA

- Chinese investment in U.S. universities raises concerns over research independence

- PBoC maintains MLF rate amid yuan pressures

ENERGY & CLIMATE CHANGE

- Tesla and BP make workforce cuts amid sluggish electric vehicle sales

- Significant shift in feedstock landscape for biomass-based diesel fuel

LIVESTOCK, NUTRITION & FOOD INDUSTRY

- In Michigan, three more dairy herds infected with H5N1 (BIAV) bird flu virus

|

MARKET FOCUS |

— Equities today: Asian and European stock indexes were mixed overnight. U.S. Dow opened higher, around 1% or 360 points. In Asia, Japan -0.7%. Hong Kong -0.7%. China +1.3%. India -1.1%. In Europe, at midday, London -0.4%. Paris +0.8%. Frankfurt +1%.

U.S. equities Friday: All three major indices lost ground on Friday and for the week. The Dow fell 475.84 points, 1.24%, at 37,983.24. The Nasdaq was down 267.10 points, 1.62%, at 16,175.09. The S&P 500 declined 75.65 points, 1.46%, at 5.123.41. The Dow lost 2.4%, marking its worst week since March 2023, while the S&P 500 tumbled 1.5% and had its worst week since October. The Nasdaq saw its third negative week in a row.

— Goldman Sachs’ profits rose 28% in the first quarter, far ahead of analysts’ estimates, boosted by its trading business and a nascent recovery in investment banking.

— Biden advises restraint to Israel amid calls for calm, market nerves ease. President Biden reportedly conveyed to Israeli Prime Minister Benjamin Netanyahu that the U.S. would not support a retaliatory strike, echoing similar calls from European nations urging Israel to avoid aggression. Iran's statement suggesting resolution has contributed to a sense of relative calm in markets on Monday.

Market reactions:

- Oil prices decline as tensions ease, with Brent crude falling below $90 per barrel.

- U.S. equities are poised for a rebound following Friday's selloff, tracking gains in European stocks.

- European gas prices also decreased.

- Treasuries and the dollar slip as market nerves ease.

- Gold: Despite bullish calls from Wall Street banks like Goldman Sachs, gold remains below record levels and down today.

— Samsung displaced Apple as the world’s biggest phonemaker in the first quarter of 2024. The South Korean firm, which had lost the top spot to its American rival in the previous quarter, shipped more than 60 million smartphones. Apple only sold 50 million, a 10% decrease over the same period last year. Global smartphone sales grew by 8% overall.

— Asahi aims for half of beverage sales from zero-alcohol drinks by 2040. Asahi, Japan's largest brewer, plans to derive half of its beverage sales from zero- and low-alcohol drinks by 2040, according to CEO Katsuki Atsushi. In an interview with the Financial Times, Atsushi outlined the company's strategy to expand its alcohol-free offerings, including brands like Peroni Nastro Azzurro and Pilsner Urquell, particularly in the American market through investments in startups. The move aims to capture the growing demand from younger, health-conscious consumers.

— Ag markets today: Corn, soybeans and wheat mildly favored the downside in relatively quiet overnight price action. As of 7:30 a.m. ET, corn futures were trading 1 to 2 cents lower, soybeans were around a penny lower, SRW wheat futures were 6 to 7 cents lower, HRW was 4 to 6 cents lower and HRS was 1 to 3 cents lower. Front-month crude oil futures were around 60 cents lower, and the U.S. dollar index was about 150 points lower this morning.

Wholesale beef prices stabilizing? Choice boxed beef prices firmed $2.20 on Friday, the second straight daily gain, and pushed back above the $300.00 level. Select beef rose 39 cents. For cattle futures and the cash cattle market to stop their recent price slides, wholesale beef prices likely need to signal a short-term low is in place.

Modest premium in May hog futures. May lean hog futures took over lead-month status last Friday at a $3.315 premium to the CME lean hog index, which is up another 72 cents to $90.56 as of April 11. The five-year average was an $8.14 rise in the cash index from now until mid-May, when the May contract will be cash settled.

— Agriculture markets Friday and for the week:

- Corn: May corn futures surged 6 3/4 cents to $4.35 1/2, gaining 1 1/2 cents on the week.

- Soy complex: May soybeans rallied 14 3/4 cents to $11.74 but marked a weekly loss of 11 cents, while May soymeal surged $8.80 to $344.40, picking up $11.30 on the week. May soyoil fell 13 points to 45.89 cents and lost 300 points week-over-week.

- Wheat: May SRW futures rallied 4 1/4 cents to $5.56, though lost 11 1/4 cents on the week. May HRW futures jumped 6 1/2 cents to $5.89 3/4, marking a 7 1/2 cent gain on the week. May HRS futures rose 5 3/4 cents to $6.42 3/4 but lost 5 1/4 cents on the week.

- Cotton: May cotton fell 75 points to 82.62 cents and marked a 363-point weekly loss.

- Cattle: Weak cash prices and slumping equity indexes seemed to sink cattle futures Friday. Nearby April fed cattle fell $1.35 to $178.90, while most-active June sank $2.425 to $171.475. That latter close marked a weekly drop of 57.5 cents. May feeder futures plunged $3.95 to $234.20, which left the contract $3.975 below last Friday’s close.

- Hogs: The April contract expired at noon, having dipped 57.5 cents to settle at $90.875. Most-active June futures plunged $3.725 to $102.075. The closing quote marked a weekly drop of $5.825.

— Quotes of note:

- Fedspeak. The communication blackout period around the next FOMC meeting will go into effect at midnight on Saturday, April 21 and last through midnight on Thursday, May 2. The coming week will be the last opportunity for Fed policymakers to speak in public about their respective outlooks for monetary policy.

- European Central Bank set for June interest rate cut, further reductions hinge on inflation trends. Danske Bank Research's ECB analyst, Piet Haines Christiansen, forecasts a near-certain interest-rate cut by the European Central Bank (ECB) in June. However, the extent of subsequent rate reductions will be contingent upon whether inflation moderates as anticipated or remains persistently high. Danske Bank anticipates a 25-basis point rate cut in June, followed by similar reductions once per quarter until the end of 2025. Nevertheless, the bank notes that this year, the ECB may opt for fewer than three rate cuts due to elevated domestic inflation, suggesting a cautious approach amid evolving economic conditions.

- Gold’s surge is being triggered by more than inflation, geopolitical tensions and monetary policies, Rana Foroohar writes in the Financial Times (link/paywall). And those other reasons carry deeper, long-term messages for investors.

— Retail sales jumped 0.7% in March, much higher than expected. In March 2024, retail sales in the U.S. surged by 0.7% compared to the previous month, surpassing expectations of a 0.3% increase. This follows an upwardly revised gain of 0.9% in February, indicating continued strength in consumer spending. Notable increases were observed in various sectors, including nonstore retailers (2.7%), gasoline stations (2.1%), miscellaneous store retailers (2.1%), and building materials and garden equipment (0.7%). Additionally, gains were recorded in food and beverage stores (0.5%), health and personal care stores (0.4%), and food services and drinking places (0.4%).

However, certain sectors experienced declines in sales, such as sporting goods, hobby, musical instrument, and book stores (-1.8%), clothing (-1.6%), electronics and appliances (-1.2%), general merchandise stores (-1.1%), autos (-0.9%), and furniture (-0.3%).

Excluding food services, auto dealers, building materials stores, and gasoline stations, core retail sales, which are used in GDP calculations, surged by 1.1%. This suggests a strong underlying momentum in consumer spending, which is a key driver of economic growth.

Market perspectives:

— Outside markets: The U.S. dollar index was weaker, with the euro, yen, and British pound all firmer against the U.S. currency. The yield on the 10-year U.S. Treasury note was firmer, trading around 4.57%, with a mixed tone in global government bond yields. Crude oil futures were lower but lifted off earlier lows, with U.S. crude around $84.80 per barrel and Brent around $89.60 per barrel. Gold and silver were narrowly mixed, with gold weaker around $2,373 per troy ounce and silver firmer around $28.63 per troy ounce.

— Metal prices rose after the U.S. and UK imposed new sanctions banning deliveries of Russian supplies to curb President Putin’s war-funding ability. The restrictions, which come into effect after midnight on Friday, have caused prices to spike, particularly aluminum, which surged by a record 9.4%. Russia supplies 6% of the world’s nickel, 5% of its aluminum and 4% of its copper.

— Ag trade update: South Korea purchased 133,000 MT of corn expected to be sourced from South America or South Africa.

— USDA daily export sale: 165,000 MT corn to Mexico. Of the total, 135,000 MT is for delivery during the 2023-2024 marketing year and 30,000 MT is for delivery during the 2024-2025 marketing year.

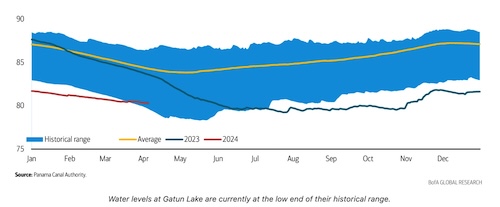

— End of Panama's dry season is approaching, bringing hope for increased vessel traffic through the Panama Canal. Despite facing challenges from El Niño-induced high temperatures, which led to Gatun Lake's water levels dropping and hindering canal operations, recent rainfall has provided some relief. The Panama Canal Authority (ACP) is cautiously optimistic about returning to normal operations by 2025, although this depends on weather conditions.

The outlook for relief lies partly in meteorological forecasts, with the possibility of La Niña conditions bringing cooler temperatures and increased precipitation, potentially easing the canal's operational challenges. However, delays in canal transit have already impacted ports like Savannah, highlighting the interconnectedness of global trade routes and infrastructure projects.

— India forecasts above-average monsoon rains. India says it is likely to receive above-average monsoon rainfall this year. The monsoon, which usually arrives over the southern tip of Kerala state around June 1 and retreats in mid-September, is expected to total 106% of the long-term average this year. Above-average rainfall could boost the farm sector and wider economic growth, helping to bring down food price inflation.

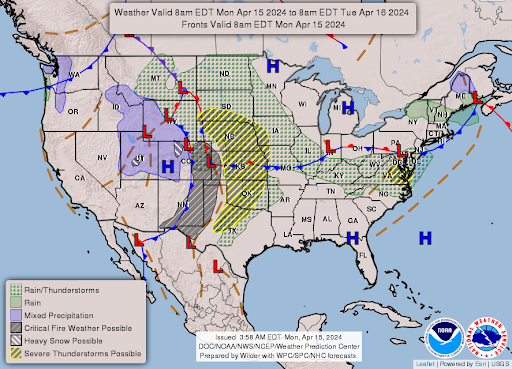

— NWS weather outlook: Intensifying storm system to bring the threat of severe weather and isolated flash flooding to the Plains Monday, followed by the Mississippi Valley on Tuesday... ...Scattered thunderstorms, including the threat for some severe weather, from the Upper Ohio Valley east through the Mid-Atlantic Monday... ...Moderate to locally heavy snowfall expected over the next couple of days for higher elevations of the northern Cascades, northern/central Rockies, and eastern Great Basin... ...Well above average temperatures across the Central/Eastern U.S; Critical Risk of Fire Weather for the central/southern High Plains Monday.

Items in Pro Farmer's First Thing Today include:

• Grains weaker to start the week

• Big temperature swing, but no damaging cold

• Final phase of Brazil’s rainy season

• March NOPA soy crush expected to be highest ever

|

BALTIMORE BRIDGE COLLAPSE |

— FBI opens criminal investigation on the container ship that took down Baltimore’s Francis Scott Key Bridge last month, looking to determine if the ship’s crew left the port knowing the vessel was troubled. Officials are reviewing the events that led up to the Dali container ship colliding with one of the key bridge’s support pillars, two U.S. officials with knowledge of the matter told the Washington Post. “The FBI is present aboard the cargo ship Dali conducting court authorized law enforcement activity,” the agency said in a statement Monday morning.

|

CONGRESS |

— Energy Secretary Jennifer Granholm will appear before the Senate Energy and Natural Resources panel tomorrow. Senators likely will question her about the Biden administration’s pause on new LNG export applications, as well as implementation of the 2022 climate-tax-health law.

— Rep. Andy Harris decides to maintain role as chair of Appropriations Agriculture Subcommittee. Amid changes in House Appropriations Committee leadership, Rep. Andy Harris (R-Md.) confirmed his decision to retain his position as chair of the Agriculture subcommittee. Following the leadership transition, speculation arose regarding lawmakers' interest in assuming leadership of the Homeland Security subcommittee. However, Rep. Harris's announcement affirms his commitment to continuing his role within the Agriculture subcommittee.

|

RUSSIA/UKRAINE |

— Ukraine’s oilseed production expected to fall around 3%. Ukraine’s oilseed output is likely to fall by around 3% this year to 21 MMT mostly due to a smaller sunflower seed harvest, analyst APK-Inform quoted the Ukrainian vegetable oil association Ukroliyaprom as saying. Ukroliyaprom said sunflower seed output may decrease 4.8% to 12 MMT and rapeseed production could decline by 4.8% to 4 MMT, while soybeans could rise 4.2% to around 5 MMT.

— UN nuclear watchdog welcomes cold shutdown of Zaporizhzhia reactors amid fragile situation. The UN International Atomic Energy Agency (IAEA) welcomed the cold shutdown of all six nuclear reactor units at the Zaporizhzhia nuclear power plant in Russia-held territory. Director General Rafael Grossi emphasized the long-standing recommendation for this action, stating it enhances overall safety at the facility. While the plant endured drone attacks, resulting in damage to a reactor building, the IAEA assures that nuclear safety was not compromised. However, Grossi warns that despite the shutdown, the situation at the plant remains "extremely fragile," with ongoing concerns regarding recent deterioration.

|

POLICY UPDATE |

— Rural discontent fuels far-right surge in European politics. There is simmering discontent among farmers across Europe, who feel marginalized and frustrated with a host of issues, from economic pressures to environmental regulations, according to the Washington Post (link). Their anger has manifested in protests and blockades, drawing attention from both centrist politicians and the far right. For centrist politicians, the farmers' fury presents a challenge, as their traditional support base seems to be slipping away amid dissatisfaction with policies related to agriculture, trade, and the environment. The far right, however, sees an opportunity to capitalize on this discontent, positioning themselves as champions of agricultural interests and portraying themselves as defenders of traditional values against urban elites and globalism.

Far-right figures like Marine Le Pen in France and Geert Wilders in the Netherlands have eagerly embraced the farmers' grievances, aligning themselves with the agricultural protest movement to broaden their appeal and further their nationalist agendas. They have strategically adjusted their positions, even supporting policies like pesticide use that they previously opposed, to align more closely with farmer concerns.

These political maneuvers have not gone unnoticed by farmers, many of whom feel disillusioned with mainstream political leaders and are increasingly drawn to the promises of the far right. Despite concessions and promises from both national and EU leaders to address some of their grievances, there remains a pervasive sense of distrust and rejection of established political institutions.

The upcoming European Parliament elections loom large in this context, with early polls suggesting significant support for far-right parties. The outcome of these elections may signal a broader shift towards right-wing politics across Europe, fueled in part by the mobilization of disaffected farmers.

|

CHINA UPDATE |

— Chinese investment in American universities raises concerns over research independence. A report by the Wall Street Journal (link) reveals a significant flow of Chinese money into American universities through research and training contracts. These agreements, valued at $2.32 billion between 2012 and 2024, have prompted concerns among policymakers and universities about maintaining research independence while engaging with Chinese businesses. With nearly 200 U.S. colleges and universities involved in such contracts, the dilemma arises over striking a balance between fostering academic research and avoiding empowerment of a U.S. rival.

— PBoC maintains MLF rate amid yuan pressures. The People's Bank of China (PBoC) maintained the rate on CNY 100 billion worth of one-year policy loans, known as the medium-term lending facility (MLF), at 2.5% on April 15th. This decision was made in efforts to prioritize the stability of the yuan, especially as the local currency faces renewed depreciation pressure. Despite a net CNY 70 billion cash withdrawal from the banking system, the central bank opted for this move amid the expiration of CNY 170 billion worth of MLF loans this month, marking the second consecutive month of withdrawals.

This operation occurred despite muted Consumer Price Index (CPI) readings last month, which led to calls for more stimulus from Beijing. Chinese policymakers are navigating economic risks while addressing policy divergence from the US, where inflation remains elevated. Some observers suggest that the PBoC's preference for utilizing Reserve Requirement Ratio (RRR) cuts over MLF rate cuts may be influenced by considerations related to capital flows.

Last year, Chinese authorities slashed the MLF rate twice by a cumulative total of 25 basis points (bps) to stimulate economic growth.

|

ENERGY & CLIMATE CHANGE |

— Tesla and BP make workforce cuts amid sluggish electric vehicle sales. In response to a slowdown in electric vehicle (EV) sales, Tesla plans to lay off 10% of its workforce, as revealed in a memo obtained by Reuters. This move reflects a broader trend in the EV manufacturing sector, where companies are scaling back operations due to sales not meeting expectations. Similarly, BP has trimmed over one-tenth of its EV charging business and withdrawn from several markets, including reducing the number of countries it operates in from 12 to 4. The focus now shifts to the U.S., China, Britain, and Germany. Despite these adjustments, most affected employees were able to transition to other divisions within the respective companies. These actions signal ongoing adjustments in the EV landscape, with various manufacturers adjusting their plans amidst a deceleration in sales.

— There’s been a significant shift in the feedstock landscape for biomass-based diesel fuel, particularly focusing on the growing dominance of renewable diesel production over biodiesel and the consequent change in feedstock preferences, according to three agricultural economists at the Farmdoc daily blog (link). “The recent shift toward tallow and the longer-term shift towards yellow grease and corn oil make sense given the relatively low carbon intensity (CI) scores given to renewable diesel made from these feedstocks in the California LCFS (low carbon fuel standard) program.”

The lower CI scores translate into higher dollar credit values per gallon, wrote the economists. More than 80% of renewable diesel produced in the country is consumed in California.

Highlights:

- Shift in feedstock preferences: There's a notable move away from soybean oil towards alternative feedstocks like yellow grease and corn oil in the production of renewable diesel. This shift is attributed to the lower carbon intensity scores assigned to renewable diesel made from these alternative feedstocks under programs like the California Low Carbon Fuel Standard (LCFS). Essentially, these alternative feedstocks result in higher dollar credit values per gallon due to their lower carbon intensity.

- Impact on feedstock composition: The economists emphasize the importance of considering the differing composition of feedstock usage for biodiesel versus renewable diesel when projecting total biomass-based diesel feedstock usage. As renewable diesel production increases, the overall growth of biomass-based diesel feedstock volume tends to favor feedstocks with lower carbon intensity scores, such as yellow grease.

- Current feedstock distribution: Soybean oil still holds a significant share, accounting for 42% of all feedstocks for both biodiesel and renewable diesel. However, its dominance has decreased from nearly 48% at the beginning of the decade. Yellow grease has seen an increase in share, now comprising 20% of feedstocks, with corn oil also contributing 15%.

- Renewable diesel feedstock distribution: Yellow grease emerges as the primary feedstock for renewable diesel production, constituting nearly 29% of the total, followed closely by soyoil at 27%, and corn oil at 15%.

- Biodiesel production decline: While soyoil remains the preferred feedstock for biodiesel, there's been a decline in biodiesel production in recent years, contrasted with the significant rise in renewable diesel production.

|

LIVESTOCK, NUTRITION & FOOD INDUSTRY |

— In Michigan, three more dairy herds have been infected with the H5N1 (BIAV) bird flu virus, prompting concerns about its spread across state lines. USDA has advised farmers to test their herds before moving them to prevent further transmission. The outbreak in Michigan adds to a total of 29 infected dairy herds in eight states, including Texas, New Mexico, and North Carolina. Tim Boring, Michigan's agriculture director, emphasized the importance of vigilance, noting that the virus disregards geographical boundaries.

Voluntary testing urged. While a mandatory testing program for the 26,000 U.S. dairy herds isn't feasible, the USDA's Animal and Plant Health Inspection Service (APHIS) urges voluntary testing to gather more information and prevent interstate spread.

Unlike its devastating impact on poultry, HPAI's effects on dairy cows vary. With proper veterinary care, infected cows can recover within weeks, though they may experience reduced appetite and milk production, especially older cows.

HPAI primarily spreads through wild birds, posing a heightened risk during migratory seasons. Biosecurity measures, such as restricting barn access to outsiders, are encouraged to prevent transmission through contaminated equipment or materials.

The recent detection of HPAI in livestock has prompted concerns about potential risks to swine herds. The Swine Health Information Center and the American Association of Swine Veterinarians are hosting a webinar Friday (link) to address these concerns and provide updates on influenza A virus, which includes strains found in animals.

Of note: APHIS says to continue using HPAI relative to the current situation in dairy, despite an aborted attempt by the American Association of Bovine Practioners (AABP) to change it to Bovine Influenza A Virus (BIAV). According to APHIS: “From USDA’s perspective, highly pathogenic avian influenza or H5N1 are the most scientifically accurate terms to describe this virus. This is also consistent with what the scientific community has continued to call the virus after it has affected other mammals. Since the virus is not highly pathogenic in mammals, H5N1 is the most fitting of the two scientifically correct options. As a reminder, genomic sequencing indicates there is no change to this virus that would make it more transmissible to humans, and the CDC considers risk to the public to be low.”

|

KEY LINKS |

WASDE | Crop Production | USDA weekly reports | Crop Progress | Food prices | Farm income | Export Sales weekly | ERP dashboard | California phase-out of gas-powered vehicles | RFS | IRA: Biofuels | IRA: Ag | | Russia/Ukraine war, lessons learned | | SCOTUS on WOTUS | SCOTUS on Prop 12 pork | New farm bill primer | | Gov’t payments to farmers by program | Farmer working capital | USDA Ag Outlook Forum |