House Speaker Johnson: Senate Border-Ukraine Aid Plan ‘Dead’ in House

FOMC | Jobs report | U.S./China talks | Money for advanced chips | Mayorkas impeachment | Tax measure faces hurdles

Washington Focus

The House is back in session after being off another week. The Senate is in. Key agenda items include funding for fiscal year (FY) 2024 (same issues, little progress), a possible but unlikely border security package (dead-on-arrival in the House), and a tax package that previously had momentum but is leaking some of its optimistic air. Farm bill talks are all behind-closed-doors among leaders and staff except lawmakers from both parties issuing various positioning remarks, with odds rising of no measure this year.

— On the international front, at least three American soldiers were killed in a drone strike that injured another 25 servicemembers on a military base on Sunday in northeastern Jordan, the White House said, the first U.S. deaths in the Middle East since the Oct. 7 attack on Israel by Hamas sparked a war. An unmanned aerial drone struck American troops at Tower 22, a small outpost in Jordan near the country’s border with Syria, CNN reported.

The White House said they were still gathering information about the strike, but confirmed it was carried out by a “radical Iran-backed militant groups operating in Syria and Iraq.”

The Islamic Resistance in Iraq, an Iran-backed group that includes several smaller groups such as Kataib Hezbollah, took responsibility, according to the Washington Post.

John Spencer, chair of urban warfare studies at the Modern War Institute at West Point, said the U.S. response “will be complex but if not overwhelming to all responsible, a significant blow to U.S. national security interests. Containment of the Iranian regime has not worked.”

House Speaker Mike Johnson (R-La.) said, “America must send a crystal clear message across the globe that attacks on our troops will not be tolerated.”

“Hit Iran now. Hit them hard,” wrote Sen. Lindsey Graham (R-S.C.), well-known for his hawkish views, on X. “When the Biden Administration says ‘don’t’, the Iranians ‘do’. The Biden Administration’s rhetoric is falling on deaf ears in Iran,” Graham said. “Iran is undeterred,” he said. “The only thing the Iranian regime understands is force. Until they pay a price with their infrastructure and their personnel, the attacks on U.S. troops will continue.”

— Some Senators have responded to Senate Agriculture Committee Chairwoman Debbie Stabenow's (D-Mich.) crop insurance proposal for the new farm bill. Stabenow's proposal includes offering producers an annual choice between PLC/ARC at current reference prices or a STAX-type area-wide crop insurance policy. Sen. John Boozman (R-Ark.) mentioned that the proposal has sparked a lot of discussion. Reports note Jerry Moran (R-Kan.) has concerns that the proposal suggests a choice between Title One of the farm bill and crop insurance benefits, which should not be mutually exclusive. Sen John Hoeven (R-N.D.) stated that the proposal does not provide sufficient improvements to the farm safety net to earn his support, advocating for improvements to reference prices and increased premium support under crop insurance.

Later this week we will be exploring this proposal, trying to get more information about it to assess it in a fair manner.

— House Speaker Johnson rejects Senate's border security deal. A bipartisan group of senators has reached an agreement on a solution for the border security portion of the supplemental spending bill. This bill also includes security assistance to Israel, Taiwan, and Ukraine, but the text of the bill has not been released yet.

Linkage with aid to Ukraine and Israel. In response to legislative negotiations for aid to Ukraine and Israel, Biden has expressed willingness to consider new border restrictions, even if they were previously considered unlikely for Democrats.

Key elements of the agreement involve a mandatory shutdown of the border, which would require the Department of Homeland Security to turn away most migrants attempting to cross when the average daily encounters with migrants reach 5,000 per day over a week or 8,500 in a single day. Additionally, the deal would grant the Biden administration new expulsion authority if daily encounters exceed 4,000. It also calls for the mandatory detention of all single adults and imposes a one-year ban on re-entry for migrants caught crossing the border twice during the "shutdown" phase.

However, Johnson has expressed skepticism about the proposal, stating that if the rumored contents of the draft are accurate, it would not pass in the House. He instead calls for adopting the provisions of HR 2, an immigration and border security bill passed by the House last year.

Last month, there were a record 249,785 illegal border crossings, leading to increased pressure on Biden. Former President Trump and Texas Governor Greg Abbott have been critical, with Abbott even seizing a public park along the border.

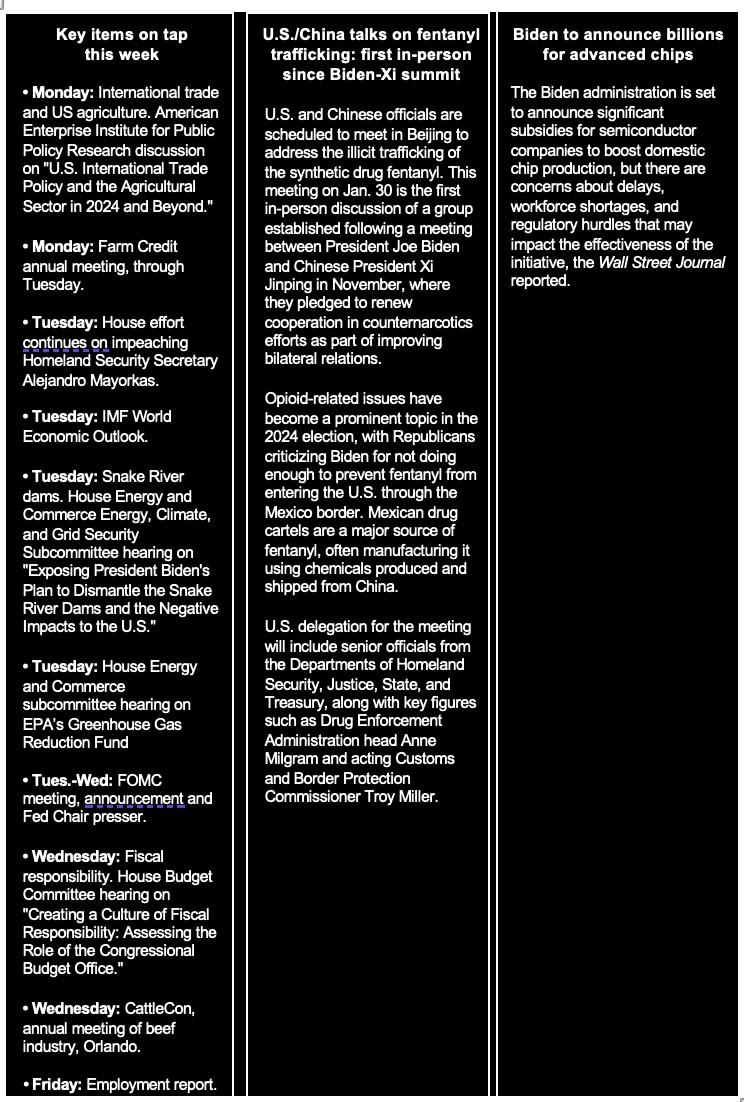

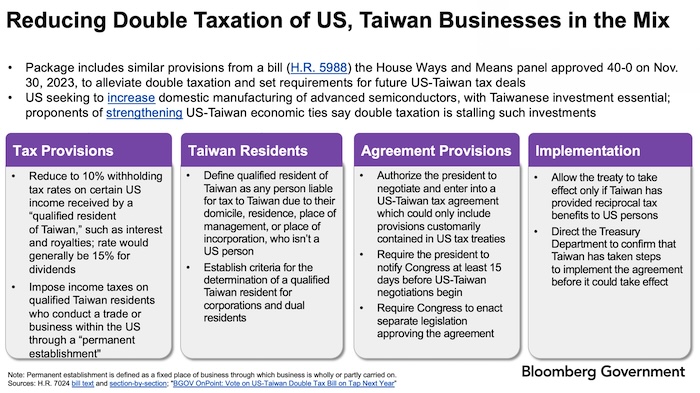

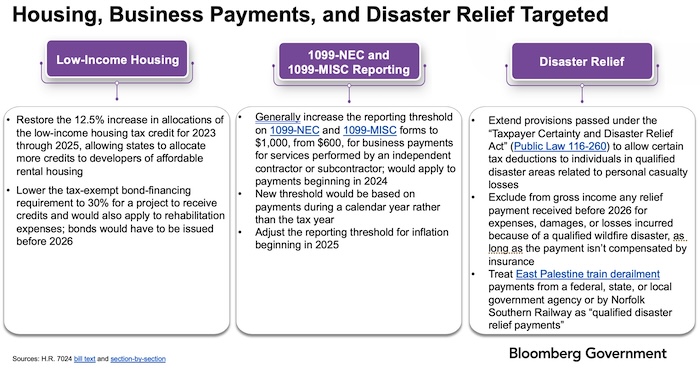

— The fate of the bipartisan tax package, valued at $78 billion and aimed at renewing business tax breaks and expanding the child tax credit, now depends on House Speaker Mike Johnson. The legislation has received criticism from conservatives who are reluctant to grant President Joe Biden a legislative victory in an election year and from some Republicans who oppose elements of the child tax credit expansion. (See below for details of the proposed tax package via Bloomberg Government.)

A likely vote under suspension of the rules would need two-thirds support to pass. The bill could come to the floor by Tuesday. If it does not make it by Wednesday, it will be punted.

Another hurdle: GOP lawmakers from high-tax states, like New York, are frustrated that the bill doesn't address the $10,000 cap on the state-and-local-tax deduction.

The Joint Committee on Taxation estimated the extension of business tax breaks would reduce federal revenue by $32.8 billion over a decade.

The expansion of the child tax credit would decrease revenue by $33.5 billion over the same period.

The cost of the package would be offset by changes to the Employee Retention Tax Credit (ERTC) program. The ERTC is a refundable credit for certain employers that paid qualified wages to some or all employees and were affected by the Covid-19 pandemic; credit can be claimed until April 15, 2025. The proposed changes include:

- Ending new ERTC claims on Jan. 31 after a public notice.

- Applying penalties for fraud and violations of due-diligence requirements. Changes to the credit and related enforcement would increase revenue by $78.8 billion over 10 years.

Of note: While the bill has received strong bipartisan support in the House Ways and Means Committee, whether it receives a floor vote depends on Speaker Johnson, who must consider the concerns of his caucus members, crucial to his job security and the Republican majority in the House. Also, lawmakers must find a legislative vehicle to attach the package to, which is typically a larger must-pass bill. There isn’t enough support to attach it to a major funding bill. Meanwhile, Senate Finance ranking member Mike Crapo (R-Idaho) said he wants changes, though he hasn’t specified details; House Ways and Means ranking member Richard Neal (D-Mass.) said the measure could be improved.

Sensitive issue: Democrats are floating an amendment to make the child tax credit fully refundable, while conservative Republicans argue the expansion is a disincentive to work.

Bottom line: While the measure contains several ag sector friendly provisions, its fate is murky at best, despite assessments by some a short time ago that it would pass both chambers. Any tax bill is the equivalent of four farm bills in one measure. Some of the major provisions:

— House to move on impeachment of Mayorkas. The House Homeland Security Committee is preparing to hold a vote Tuesday on a resolution aimed at impeaching Homeland Security Secretary Alejandro Mayorkas. If the resolution passes, it would bring Mayorkas closer to becoming only the second Cabinet secretary in U.S. history to face impeachment charges for alleged high crimes and misdemeanors. The basis for this move is the claim made by House Republicans that Mayorkas has neglected his duties in response to the increasing number of border crossings between the United States and Mexico, which have reached record highs.

House Republicans on Sunday released their articles of impeachment. The first article alleges Mayorkas participated in a "willful and systemic refusal to comply with the law," while the second article says he breached the public's trust for his handling of the southern border amid record illegal immigration numbers. The articles state that Mayorkas has "willfully and systemically refused to comply with Federal immigration laws" and "repeatedly violated laws enacted by Congress regarding immigration and border security."

After the House Homeland Security Committee's markup of the articles, they are expected to be sent to the full House for a vote. If the House votes to impeach Mayorkas, he could then go on trial in the Senate to potentially be removed. However, this is unlikely considering the body is controlled by Democrats. Some observers also note that in the unlikely event Mayorkas is impeached, any replacement would just continue the policy of the Biden administration.

— South Carolina holds its Democratic primary on Saturday, Feb. 3. While President Joe Biden doesn't have a serious challenger, his campaign hopes his efforts in the state will recharge voters and echo 2020, when South Carolina — especially its Black voters — catapulted the candidate on a path to the presidency.

The Republican primary is three weeks later, on Feb. 24.

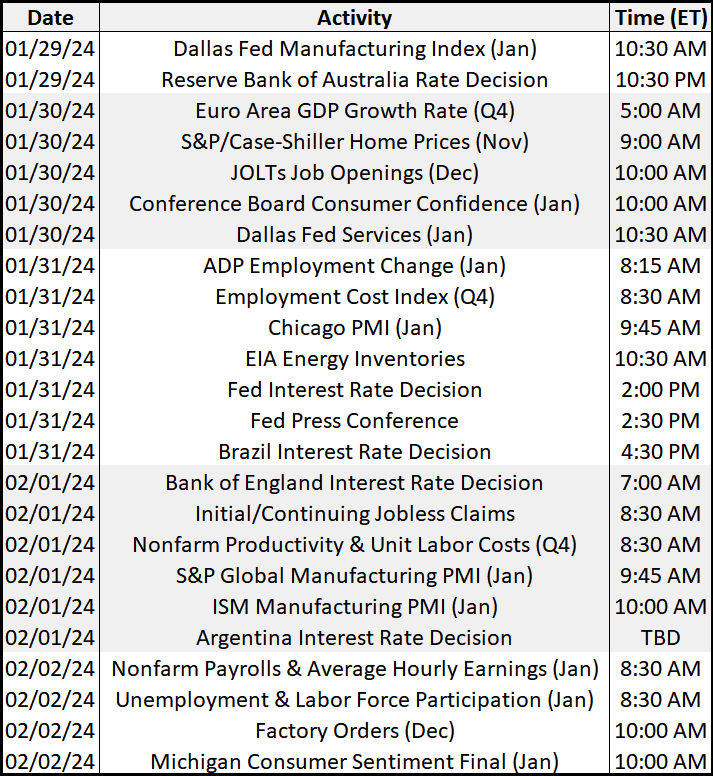

— The first Federal Open Market Committee (FOMC) meeting of 2024 is scheduled for Jan. 30-31. During this meeting, Fed policymakers are expected to keep the federal funds target rate steady at the range of 5.25% to 5.50%. This would mark the fourth consecutive meeting without a change in interest rates. Most private industry analysts think rates have reached their peak due to indications of slowing economic growth, a labor market that is rebalancing, and inflation gradually moving towards the 2% target.

The meeting statement, released at 2 p.m. ET on Wednesday, is likely to resemble the one issued on Dec. 13, reflecting a cautious approach to monetary policy, providing no hints about the timing or scale of future rate adjustments. Fed Chair Jerome Powell's press briefing at 2:30 p.m. ET on Wednesday will elaborate on the statement but most likely will stay consistent with it.

Of note: There will be no updates to the summary of economic projections (SEP) at this meeting. However, the FOMC will consider the January senior loan officer opinion survey, which will help in assessing current and future financial conditions. The survey is anticipated to be published at 2 p.m. ET on Monday, Feb. 5.

With this first meeting of the year, the FOMC will carry out some administrative tasks, including the rotation of voting rights among district bank presidents. In addition to the Board of Governors, the voting presidents for this meeting will be John Williams from New York (FOMC Vice Chair), Loretta Mester from Cleveland (retiring in June), Thomas Barkin from Atlanta, Raphael Bostic from Richmond, and Mary Daly from San Francisco.

The FOMC will not have the January employment report available for consideration during this meeting, as it will be released at 8:30 a.m. ET on Friday. The January establishment survey, which includes annual benchmark revisions, may provide insights into hiring trends, analysts note. Of particular interest may be the impact of minimum wage increases in many states, which could temporarily boost year-over-year gains in average hourly earnings, given that nearly half of the states had implemented such increases, but mostly under $1 per hour.

Bottom line: While no change is expected at this time, Fed officials think there will be three rate cuts this year, according to recent projections (many private analysts predict more cuts). The three Fed-signaled cuts would bring its target interest rate closer to 4.6% from the current range of 5.25% to 5.5%.

— Bayer's Monsanto hit with $2.2 billion Roundup verdict. A Pennsylvania jury has ordered Bayer AG's Monsanto unit to pay over $2.2 billion to a former Roundup user who attributed his cancer to the weedkiller. This verdict is the largest in five years of litigation surrounding the herbicide. John McKivison, a former landscaper, was awarded $250 million for his losses and $2 billion in punitive damages, claiming that his use of Roundup at work and at home led to his cancer.

Monsanto has won 10 out of 16 recent Roundup trials but has faced significant losses, including a $1.5 billion verdict in Missouri in November.

Bayer, which acquired Monsanto in 2018, is under substantial pressure due to the mounting liability associated with Roundup lawsuits. The company has set aside up to $16 billion to resolve over 100,000 Roundup cases. Shares of Bayer fell nearly 3% before the verdict was announced.

Bayer disagrees with the jury's verdict and plans to appeal, stating that it conflicts with scientific evidence and regulatory assessments.

Roundup users in these lawsuits allege that Monsanto was aware of research linking glyphosate, the active ingredient in Roundup, to cancer but concealed these findings. Internal Monsanto documents revealed during the litigation also indicated that the company had ghost-written scientific studies to support the safety of glyphosate.

Economic Reports and Events for the Week

The FOMC’s two-day meeting (Tues.-Wed.) and the Employment report (Fri.) are the key economic reports this week.

Monday, Jan. 29

- Dallas Fed Manufacturing Survey

Tuesday, Jan. 30

- FOMC meeting begins

- Case-Shiller Home Price Index: Forecasters see the adjusted 20-city monthly rate rising 0.4% in November which would mark a slowdown from October's as-expected 0.6% increase and September's 0.7% which was also as expected. Despite the slower monthly rate, the annual rate is expected to rise nearly a full percentage point to 5.8%.

- FHFA House Price Index: The house price index is expected to rise 0.3% in November which would match a lower-than-expected 0.3% increase in October.

- The Consumer Confidence Index is expected to rise further in January, to a consensus 112.5 versus 110.7 in December which was much higher than expected and up nearly 11 points from November.

- JOLTS: November's 8.790 million was just above consensus but below October's 8.852 million. The consensus for January is a 90,000 drop to 8.70 million.

- IMF World Economic Outlook

Wednesday, Jan. 31

- MBA Mortgage Applications

- Forecasters see ADP's January employment number at 130,000. This would compare with December growth in private payrolls reported by the Bureau of Labor Statistics of 164,000. ADP's number for December was 164,000.

- Employment Cost Index (ECI): After the third quarter's 1.1% increase, forecasters see employment costs edging lower to 1.0% in the fourth quarter. The ECI steadily moderated throughout 2023, but some economists say pay gains are still a bit high and not yet consistent with 2% inflation — the Fed’s official inflation target.

- The Chicago PMI is expected to rise in January to 48.1 versus December's lower-than-expected 46.9 that followed emergence in November from long contraction at 55.8.

- FOMC announcement: After raising the possible number of future rate cuts but keeping rates unchanged in December, the Fed against the backdrop of strong employment and solid growth is expected to once again keep rates unchanged at the January meeting. Investors will be paying close to attention to how the Fed characterizes the stance of policy, inflation’s improvement over the past several months, the economy’s recent pace of growth, and the state of financial conditions.

- Fed press conference

Thursday, Feb. 1

- Jobless claims for the Jan. 28 week are expected to come in unchanged at 214,000.

- Challenger Job-Cut Report

- Productivity and Costs: Nonfarm productivity is expected to slow to a 1.9% annualized rate in the fourth quarter versus 5.2% growth in the third quarter. Unit labor costs, which fell 1.2 in the third quarter, are expected to rise to a 2.2% rate in the fourth quarter.

- The final manufacturing PMI for January is expected to come in at 50.3, unchanged from the mid-month flash and more than 2 points higher than December.

- The ISM manufacturing index has been in contraction the last 14 months and is expected to remain so in January, at a consensus 47.4 which would be unchanged from December.

- Construction Spending has shown only limited effects from high financing rates. After rising 0.4% in November, spending in December is expected to rise 0.5%.

- Fed Balance Sheet

- Money Supply

Friday, Feb. 2

- Motor vehicle sales: Unit vehicle sales in January are expected to edge lower to a 15.7 million annualized rate from December's 15.8 million which was better than expected and one of the best rates of the last several years.

- Employment: A 170,000 rise is the call for nonfarm payroll growth in January versus 216,000 in December which was above expectations. Average hourly earnings in January are expected to rise 0.3% on the month for a year-over-year rate of 4.1%; these would compare with December's rates of 0.4% and 4.1% which were both higher than expected. January's unemployment rate is expected to rise to 3.8% from December's 3.7% which was lower than expected.

- Consumer Sentiment is expected to end January at 78.8, unchanged from the preliminary reading and up a substantial 9.1 points from December which itself was up 8.4 points from November for the biggest two-month gain since the end of the 1991 recession.

- Factory Orders are expected to rise 0.4% in December versus November's 2.6% decline that reflected an upswing in commercial aircraft. Durable goods orders for December, which have already been released and are one of two major components of this report, were unchanged on the month.

Key USDA & international Ag & Energy Reports and Events

The United Nations will publish its monthly global food price index on Friday, Feb. 2. Weekly USDA data on grain exports and ethanol production will also be in focus.

On the energy front, Baker Hughes holds its annual meeting in Florence, Italy on Jan. 29. The list of speakers includes top Baker Hughes executives, representatives from Saudi Aramco (ARMCO), and the Saudi energy minister. Also, major energy companies will unveil earnings for 4Q 2023 during the week, including Shell, Chevron and Exxon Mobil. Meanwhile, the OPEC+ alliance’s Joint Ministerial Monitoring Committee meets virtually on Thursday.

Monday, Jan. 29

Ag reports and events:

- Export Inspections

- Livestock and Meat Domestic Data

- Egg Products

Energy reports and events:

- Baker Hughes annual meeting in Florence (through Jan. 30).

Tuesday, Jan. 30

Ag reports and events:

- Weekly Weather: State Stories

- EU weekly grain, oilseed import and export data

Energy reports and events:

- API weekly U.S. oil inventory report

- Baker Hughes annual meeting in Florence (last day)

- North Sea programs for March due

- BNEF transport/energy/technology summit, San Francisco (through Jan. 31)

- Earnings: Marathon Petroleum 4Q

Wednesday, Jan. 31

Ag reports and events:

- Broiler Hatchery

- Agricultural Prices

- Capacity of Refrigerated Warehouses

- Cattle

- Sheep and Goats

- Malaysia’s January palm oil exports

Energy reports and events:

- EIA weekly U.S. oil inventory report

- U.S. weekly ethanol inventories

- Genscape weekly crude inventory report for Europe’s ARA region

- UK releases fuel consumption data for 4Q 2023

- Brent March futures expire

- BNEF transport summit, San Francisco (final day)

- Earnings: Phillips 66 4Q, FY 2023; Hess Corp. 4Q

Thursday, Feb. 1

Ag reports and events:

- Weekly Export Sales

- Cotton System Consumption and Stocks

- Fats and Oils: Oilseed Crushings, Production, Consumption

- Flour Milling Products

- Grain Crushings and Co-Products Production

- Port of Rouen data on French grain exports

- Holiday: Malaysia

Energy reports and events:

- EIA natural gas storage change

- Insights Global weekly oil product inventories in Europe’s ARA region

- China Petroleum & Chemical Industry Federation to release 2024 outlook in Beijing

- Singapore onshore oil-product stockpile weekly data

- OPEC+ JMMC

- Earnings: Shell Plc 4Q

Friday, Feb. 2

Ag reports and events:

- CFTC Commitments of Traders report

- Peanut Prices

- Milk Cows and Production, Statistical Bulletin

- Sheep and Goats, Statistical Bulletin

- UN’s FAO food price index and grain supply and demand reports

Energy reports and events:

- Baker Hughes weekly U.S. oil/gas rig counts

- ICE weekly Commitments of Traders report for Brent, gasoil

- Earnings: Chevron Corp. 4Q; Exxon Mobil Corp. 4Q; Imperial Oil Ltd. 4Q; LyondellBasell 4Q

|

KEY LINKS |

WASDE | Crop Production | USDA weekly reports | Crop Progress | Food prices | Farm income | Export Sales weekly | ERP dashboard | California phase-out of gas-powered vehicles | RFS | IRA: Biofuels | IRA: Ag | Student loan forgiveness | Russia/Ukraine war, lessons learned | Russia/Ukraine war timeline | Election predictions: Split-ticket | Congress to-do list | SCOTUS on WOTUS | SCOTUS on Prop 12 pork | New farm bill primer | China outlook | Omnibus spending package | Gov’t payments to farmers by program | Farmer working capital | USDA ag outlook forum | Debt-limit/budget package |